TAX 9863 Study Guide - Final Guide: Internal Revenue Code

Document Summary

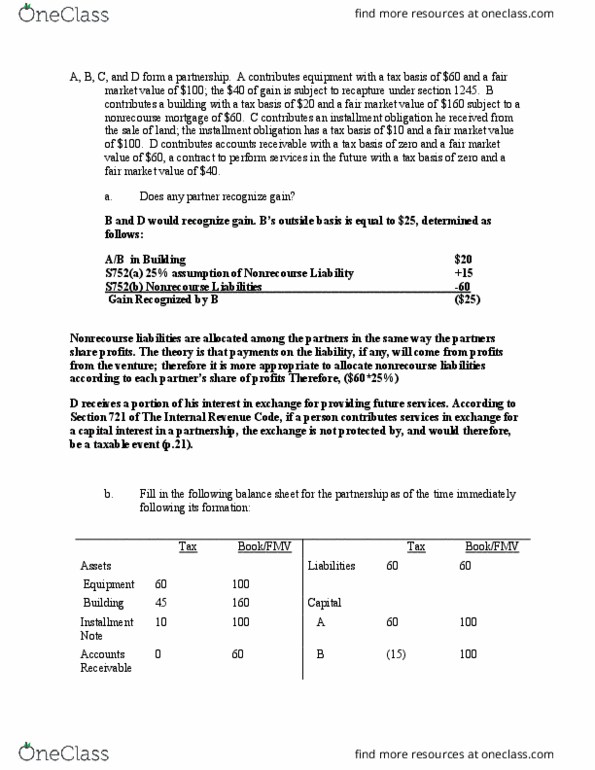

Jerry contributes a building with a tax basis and a fair market value and inventory (in jerry"s hands) with a tax basis and a fair market value. Elaine contributes land with a tax basis and an fair market value and of cash. Jerry purchased the building four months prior to the formation of the partnership. The partnership spends of its cash on legal and filing fees for organizing the partnership. No gain is recognized upon the formation of the partnership according to section. This section discusses the nonrecognition rule which states, except in the case of certain investment partnerships, S721 protects both the partnership and its partners from recognizing any gain or loss on the transfer of property to a partnership in exchange for an interest in the partnership. According to section 723, the partnership takes a transferred basis in the contributed property equal to that of the contributing partner.