BUS 201 Study Guide - Quiz Guide: Cash Cash, Accounts Receivable, Operating Expense

Document Summary

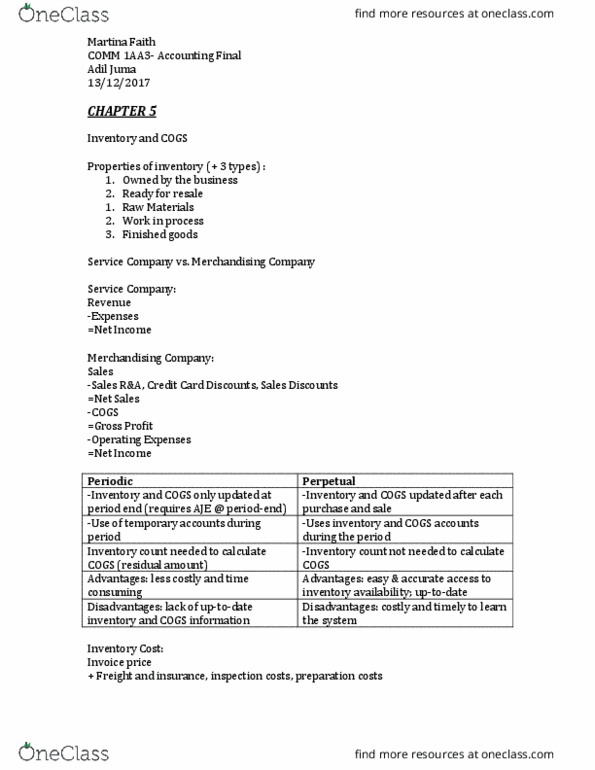

Merchandising companies: buy and sell goods to earn revenue (sales) Income measurement for merchandisers: sales revenue-cost of goods sold=gross profit-operating expenses=net income (loss) Perpetual inventory system: keep detailed records of purchases and sales; cogs determined with each sale. Periodic inventory system: no detailed records kept; cogs determined at end of period. Freight terms: fob shipping point- buyer pays freight costs ownership passes to buyer when freight carrier accepts goods from seller, fob destination- seller pays freight costs (operating expense) Ownership remains with seller until goods are delivered to buyer. Purchase return : cash refund or credit granted to buyer for returning goods. Purchase allowance : price reduction granted for keeping the inferior goods. Sales returns and allowances : contra-revenue account; normal balance is a debit. Sales discounts : contra-revenue account; normal balance is a debit. Multi-step income statement : gross profit, income from operations, and net income.