ECONOM 1014 Study Guide - Quiz Guide: Demand Curve, Economic Surplus, Comparative Advantage

Document Summary

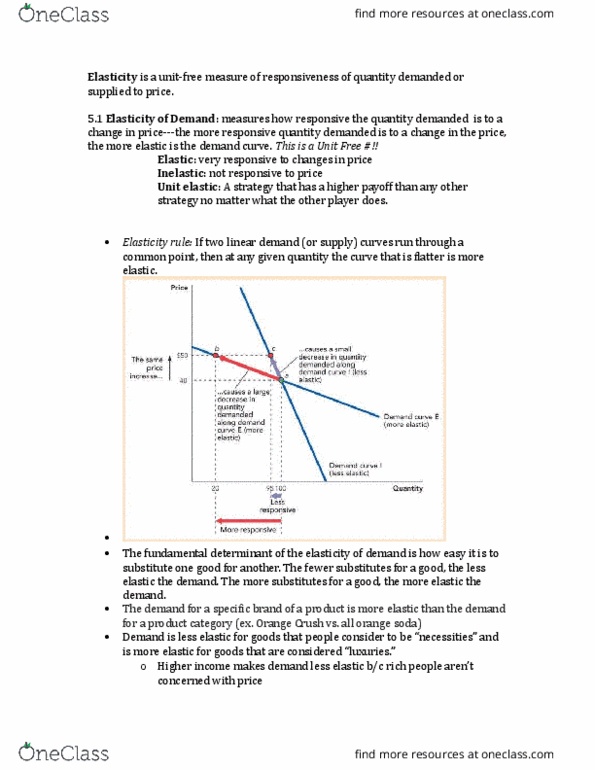

Factors: change in per unit costs w/ increased productions (more expensive=inelastic), time (expanding capacity over time=elastic), share of market for inputs (expansion causes significant increase in demand/price=elastic), geographic scope (wider scope-national=inelastic) Inelastic: difficult to increase reduction at constant unit cost, short run, large share of market, global supply: elastic: easy to increase production at constant, long run, small share of market, local supply. Factors: availability of substitutes (fewer inelastic); time (less time to adjust means inelastic); category of product (less specific-fewer substitutes-inelastic); necessities vs. luxuries, purchase size (relative to budget luxuries more sensitive to price change) Elastic: p and r move opposite >1. Unit elastic: p moves but r stays the same =1. Excess supply/surplus: price is high, too many sellers and not enough buyers: area above equilibrium price and below demand curve, consumer surplus: max price willing to pay - market price. Gains from trade: producer surplus + consumer surplus; willingness to pay for last unit = marginal cost.