EC 110 Study Guide - Midterm Guide: Average Variable Cost, Marginal Revenue, Marginal Cost

27 Mar 2019

School

Department

Course

Professor

CH. 13 PRODUCTION AND COSTS

Def. and Concepts.

total revenue

the amount a firm receives for the sale of its output

total cost

the market value of the inputs a firm uses in production

profit

total revenue minus total cost

explicit costs

input costs that require an outlay of money by the firm

implicit costs

input costs that do not require an outlay of money by the firm

economic profit

total revenue minus total cost, including both explicit and implicit costs

accounting profit

total revenue minus total explicit cost

production function

the relationship between quantity of inputs used to make a good and the quantity of output of that good

marginal product

the increase in output that arises from an additional unit of input

diminishing marginal product

the property whereby the marginal product of an input declines as the quantity of the input increases

fixed costs

costs that do not vary with the quantity of output produced

variable costs

costs that vary with the quantity of output produced

average total cost

total cost divided by the quantity of output

average fixed cost

fixed cost divided by the quantity of output

average variable cost

variable cost divided by the quantity of output

marginal cost

the increase in total cost that arises from an extra unit of production

efficient scale

the quantity of output that minimizes average total cost

economies of scale

the property whereby long-run average total cost falls as the quantity of output increases

diseconomies of scale

the property whereby long-run average total cost rises as the quantity of output increases

constant returns to scale

the property whereby long-run average total cost stays the same as the quantity of output change

What are explicit costs and implicit costs?

explicit costs

input costs that require an outlay of money by the firm (wages, costs, accounting costs) wages a firm pays its workers

implicit costs

input costs that do not require an outlay of money by the firm: opportunity costs (forgone earnings) wages the firm owner gives up by working in

the firm rather than taking another job

Calculating accounting and economic profit.

accounting profit

total revenue minus total explicit cost (revenue - explicit costs)

economic profit

total revenue minus total cost, including both explicit and implicit costs (accounting profit - implicit costs)

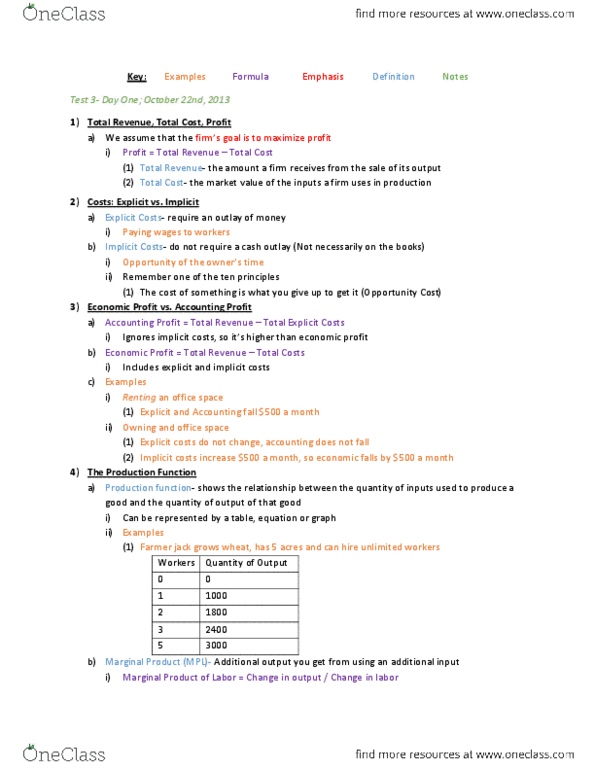

What is a production function and what is marginal product?

production function

the relationship between quantity of inputs used to make a good and the quantity of output of that good

Marginal product

Output that results from one additional unit of a factor of production (such as a labor hour or machine hour), all other factors remaining

constant. Whereas the marginal cost indicates the added cost incurred in producing an additional unit of output, marginal product

indicates the added output accruing to an additional input. Since marginal product is measured in physical units produced, it is

also called marginal physical product.

Calculating marginal product of labor (MPL).

Total change in total product divided total change in variable input

What is diminishing MPL and why does it occur?

the property whereby the marginal product of an input decreases as the quantity of the input increases

The falling MPL is due to the law of diminishing marginal returns. The law states, ”as units of one input are added (with all other

inputs held constant) a point will be reached where the resulting additions to output will begin to decrease; that is marginal

product will decline” The law of diminishing marginal returns applies regardless of whether the production function exhibits

increasing, decreasing or constant returns to scale. The key factor is that the variable input is being changed while all other factors

of production are being held constant. Under such circumstances diminishing marginal returns are inevitable at some level of

production.

Diminishing marginal returns differs from diminishing returns. Diminishing marginal returns means that the marginal product of

the variable input is falling. Diminishing returns occur when the marginal product of the variable input is negative. That is when a

unit increase in the variable input causes total product to fall. At the point that diminishing returns begin the MPL is zero

Calculate or determine FC, VC, TC, AFC, AVC, ATC and MC.

Addition, subtraction, division, multiplication of given.

Some of the firm's costs, called variable costs , change as the firm alters the quantity of output produced. Conrad's variable costs include

the cost of coffee beans, milk, sugar, and paper cups: The more cups of coffee Conrad makes, the more of these items he needs to buy.

Similarly, if Conrad has to hire more workers to make more cups of coffee, the salaries of these workers are variable costs. The fourth

column of the table shows Conrad's variable cost. The variable cost is 0 if he produces nothing, $0.30 if he produces 1 cup of coffee, $0.80 if

he produces 2 cups, and so on.

How they all appear on a graph.

x

Marginal cost eventually rises with the quantity of output.

x The average-total-cost curve is U-shaped.

x The marginal-cost curve crosses the average-total-cost curve at the minimum of average total cost.

Relationship between MC and ATC and the Efficient Scale.

It is important to understand the relationship between the ATC curve and the MC curve. When marginal cost is below the ATC

curve, the average total cost is falling. When the marginal cost is above the ATC curve (Figure 1), the average total cost is rising.

This means that the MC curve crosses the ATC curve at the minimum point on the ATC curve, indicating the firm's efficiency scale.