[MGMT 30A] - Final Exam Guide - Ultimate 25 pages long Study Guide!

7

MGMT 30A Full Course Notes

Verified Note

7 documents

Document Summary

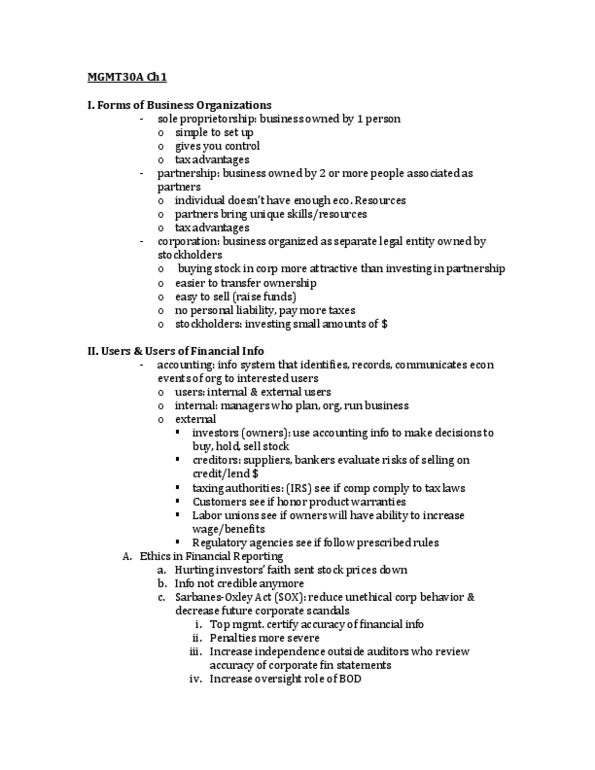

Sole proprietorship: owned by one person: simple to establish, owner controlled, tax advantages. Partnership: owned by two or more persons, not enough economic resources, partners bring unique skills or resources: simple to establish, shared control, tax advantages. Corporation: separate legal entity owned by stockholders, pay higher taxes: easier to transfer ownership, easier to raise funds, no personal liability. Accounting: information system that identifies, records, and communicated the economic events of an organization to interested users. Internal users: managers who plan, organize, and run a business, marketing managers, production supervisors, finance directors, and company officers. External users: investors, creditors, taxing authorities, customers, labor unions, regulatory agencies. Creditors: persons or entities that the business owes money to. Liabilities: amounts owed to creditors in form of debt or other obligations. Common stock: total amount paid by stockholders for the shares they purchase, sells new shares of stock. Generally accepted accounting principles (gaap): rules of accounting.