ACCT1000 Chapter Notes - Chapter 4: Income Statement

23 Jan 2019

School

Department

Course

Professor

Document Summary

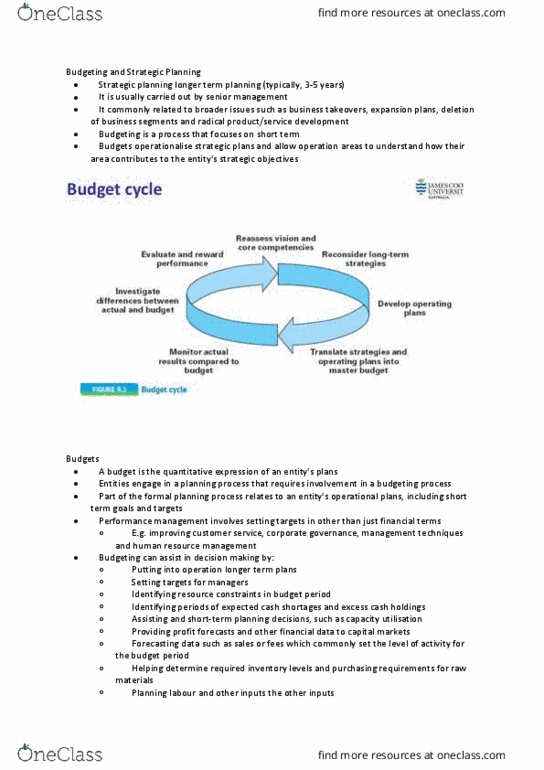

Budgets are financial plans commonly for short-term goals. Some plans are financial and some are non-financial. These non-financial measures can be developed at two measures: first, the broader level measures, which are referred to as critical success factors (csfs) second, the more specific operational measures suitable to specific segments or activities of the entity. For many entities the annual budget process may take up to nine months before the budget is finalised. In larger entities, there will be a budget committee that coordinates the preparation of the budget. When not executed well, the budgeting process can produce negative, unintended consequences. The types of budget varies from the nature and types of the entity. The budgets commonly prepared are: sales and budgets (operating) expenses budget. It is commonly used for the planning of expected futures cash receipts and cash payments. A cash budget is necessary in preparation of the master budget. The first one relates to the style of budgeting process.