BSB113 Chapter Notes - Chapter 3: Flash Memory, Demand Curve, Cellular Network

Document Summary

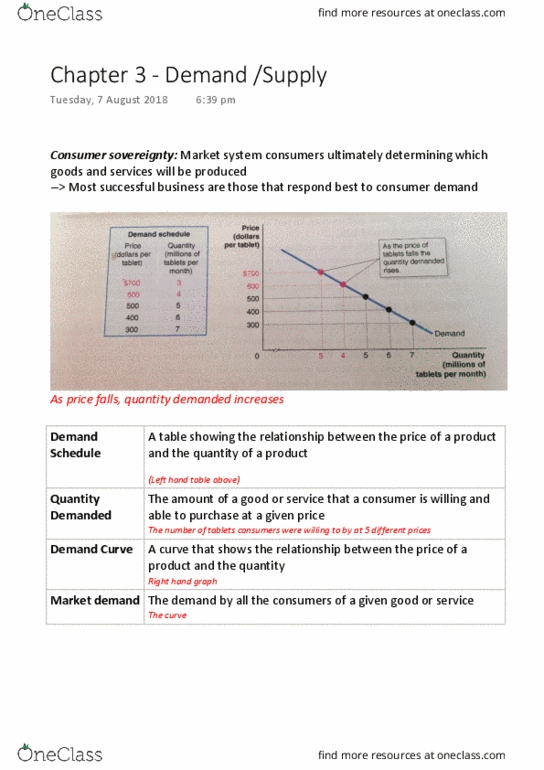

Supply: many variables influence the willingness and ability of firms to sell a good or service. Quantity supplied: the amount of service or good that firm is willing and able to supply at a given price. Price of good rises producing good is more. Price of good falls producing good is less. Marginal costs: over devoting resources to the production of goods results in increasing marginal costs. Therefore firms will require higher prices to cover increased costs. Supply schedule: table that shoes the relationship between the price of a product and the quantity of the product supplied. Price of a good rises the greater the supply. Supply curve: a curve that shoes the relationship between the price of a product and the quantity of the product supplied. Holding everything else constant + increasing price = increase in quantity supplied. Holding everything else constant + decreasing price = decrease in quantity supplied.