ACCT2331 Chapter Notes - Chapter 18: Capital Allowance, Ordinary Income, Small Business

Document Summary

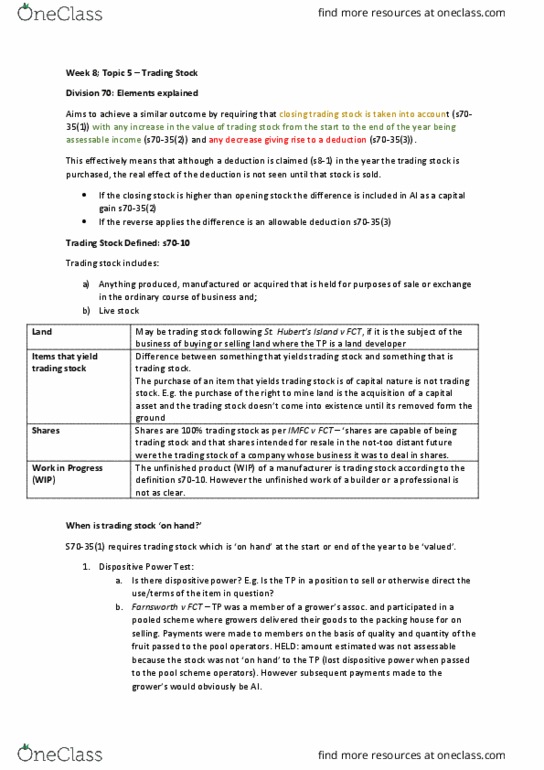

18. 1 introduction [p462: trading stock is a revenue asset, trading stock transactions are therefore dealt with under the general tax rules: Proceeds from the sale of trading stock constitute ordinary income (assessable under s 6-5) Expenditure incurred in purchasing trading stock is an outgoing necessarily incurred in carrying on a business general deduction (deductible under s 8-1: trading stock expressly deemed not to be of a capital nature (s 70-25) 18. 2 meaning of trading stock: whether an item is trading stock depends on the purpose for which it is held, not its underlying nature [p462, trading stock includes: [p461] That is held for purposes of manufacture, sale or exchange. In the ordinary course of business: trading stock can include: (more examples on p462) Land held by a developer (fc of t v st hubert"s pty ltd) Shares held by a share trader (investment and merchant finance corp limited)