ACCO 330 Chapter Notes - Chapter 3: Financial Statement, Gross Margin

21 Feb 2017

School

Department

Course

Professor

Document Summary

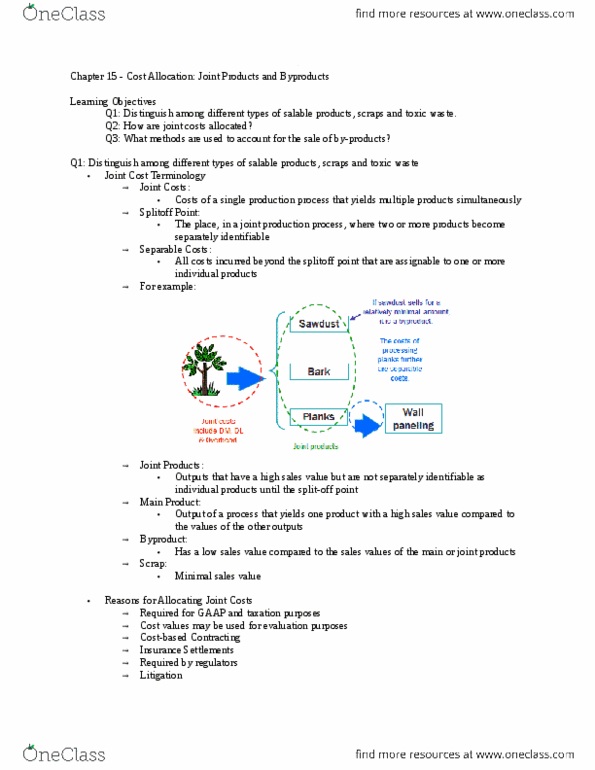

Chapter 3 cost allocation: joint products and by-products. Required for financial statements (inventoried costs and cogs) and for tax purposes. Also required for internal purposes (economic decisions, assess financial performance) Joint costs: costs which are incurred for all products simultaneously. Broken up into individual products at the split off point. Individual products are processed further with separable costs to make an improved product. Joint products: outputs with a high sales value but not separately identifiable as individual products until the split off point. Separable costs: costs incurred after the split off point and are assignable to individual products. By-product: low sales value compared to main or joint products. Market-based data ex: revenues, 3 methods: sales value at split off. Allocates joint costs on base of the relative sales value at the split-off point of total production for each product. Costs are allocated to products in proportion to their revenue-generating power.