COMM 217 Chapter Notes - Chapter 1-13: Asset, Dividend Yield, Inventory Turnover

4 Mar 2016

School

Department

Course

Professor

Document Summary

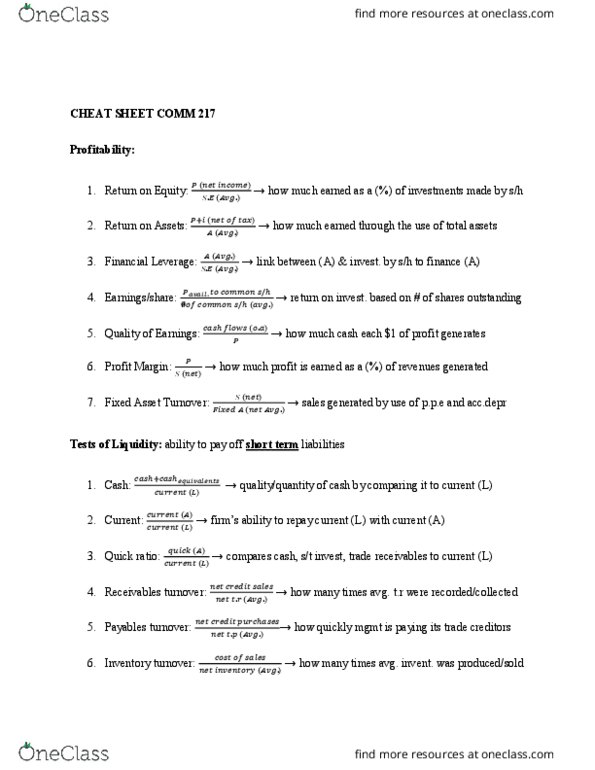

High ratio = effective management of its shareholders investments, rising share price. Measures how much the firm has earned from the use of its total assets. Measures the relationship between the assets and the investments made by shareholders to finance them. Low ratio = a high proportion of assets is financed with shareholder"s equity low = good. High = more risk, more reliance on debt. Measures the return on investment based on the number of shares outstanding. Determines if the company if profitable or not. Measures how much cash each dollar of profit generates. High ratio = a greater ability to finance operating and other cash needs from operating cash inflows. Measures how much profit is earned (after expenses) as a percentage of revenues generated during the period. High ratio = effective management of sales and expenses. How much profit is made after covering cogs.