ACCT-4021EL Chapter Notes - Chapter 3: Liability Insurance

54 views2 pages

Document Summary

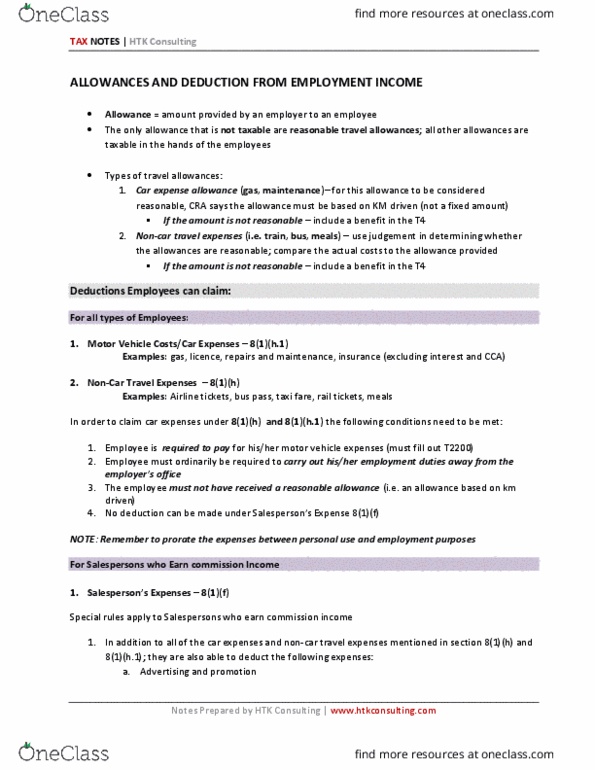

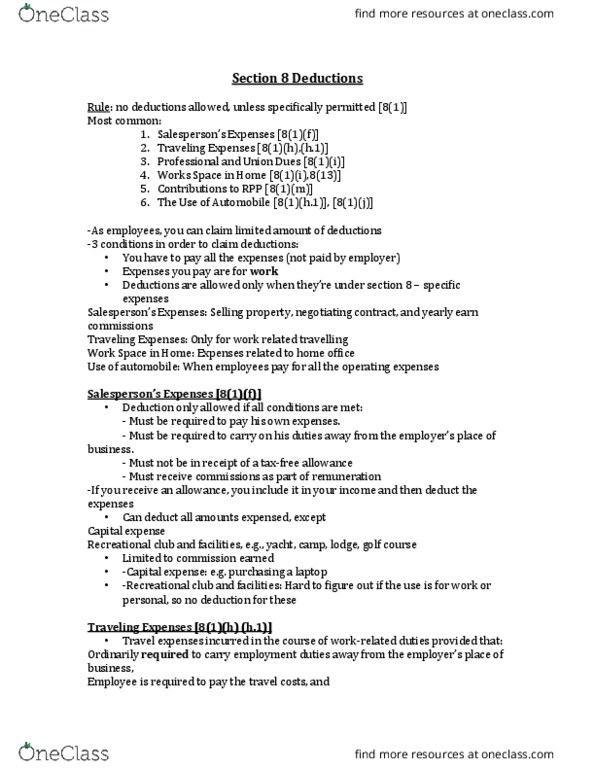

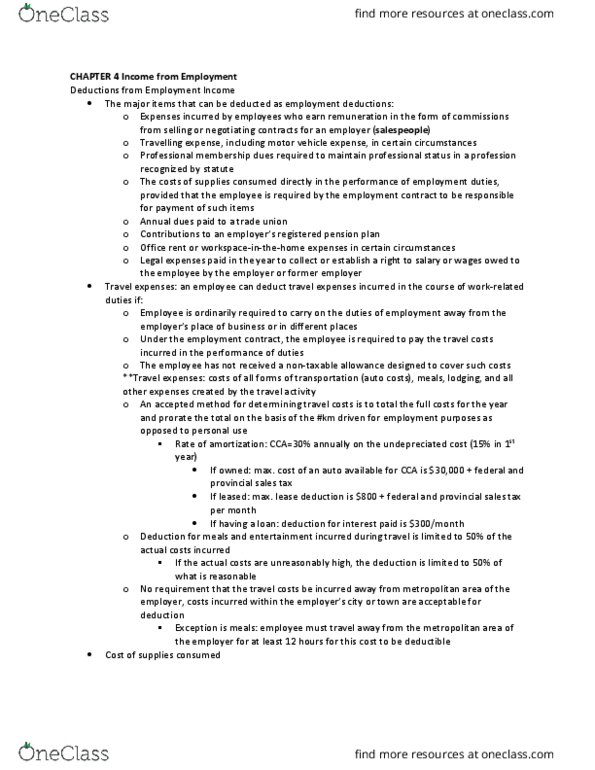

Individual employees who are involved with the selling of property or the negotiating of contracts are permitted to deduct all expenses that can be considered necessary to the performance of their duties. In order to be eligible to deduct salesperson"s expenses, all the following conditions must be met: person must be required to pay their own expenses, and the employer must sign form. Items that can be deducted under ita 8(1)(f) include: Meals with clients (we will assume that, subject to the 50% limitation, the full cost of meals with clients would be deductible) Motor vehicle costs (other than cca and interest) Except in the case of an automobile or aircraft, an employee who is a salesperson cannot deduct. Cca or interest on funds borrowed to acquire capital assets. All of the travel and motor vehicle costs that a salesperson could deduct under ita 8(1)(h) and (h. 1) could also be deducted using ita 8(1)(f).

Get access

Grade+20% off

$8 USD/m$10 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

40 Verified Answers

Class+

$8 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

30 Verified Answers

Related Documents

Related Questions

1. If a taxpayer works for two separateemployers, how much in FUTA taxes is each employer responsible toremit in the name of the taxpayer? (Points : 1) Only the first employer isrequired to remit FUTA taxes on the wages earned from the firstjob.

Both employers must remit FUTAtaxes on the first $7,000 in wages they pay to the taxpayer.

The first employer remits 5.4%on the first $7,000 in wages while the second employer remits only.8% on the first $7,000 in wages to equal the 6.2% rate.

The first employer remits FUTAtax on the first $7,000 in wages and the second employer remitsFUTA tax on the next $7,000 in wages.

$500. $800. $1,000. |

Rollovers are permitted only inunusual circumstances. A tax-free rollover can be madefrom a traditional IRA to another traditional IRA. A tax-free rollover can be madefrom a traditional IRA to a Roth IRA. |

Qualified education expensesinclude required tuition, fees, books, supplies, and equipment atan eligible educational institution. Qualified expenses must bereduced by scholarships or other tax-free income. All of the above. |

$1,200. $1,260. $6,300. |

Employees who received over$85,000 compensation in the previous year. Employees who were in the top25% of employees based on compensation. None of the above. |

$1,400. $1,600. $1,650. |

Directly to the authorizeddepository on the same day the Form 941 is mailed. Directly to the InternalRevenue Service when they file Form 941. Directly only if they use theEFTPS form of payment before Form 941 is filed. |

$350 $825. $1,375 |

Federal withholdingtaxes. Unemployment taxes. All of the above. |