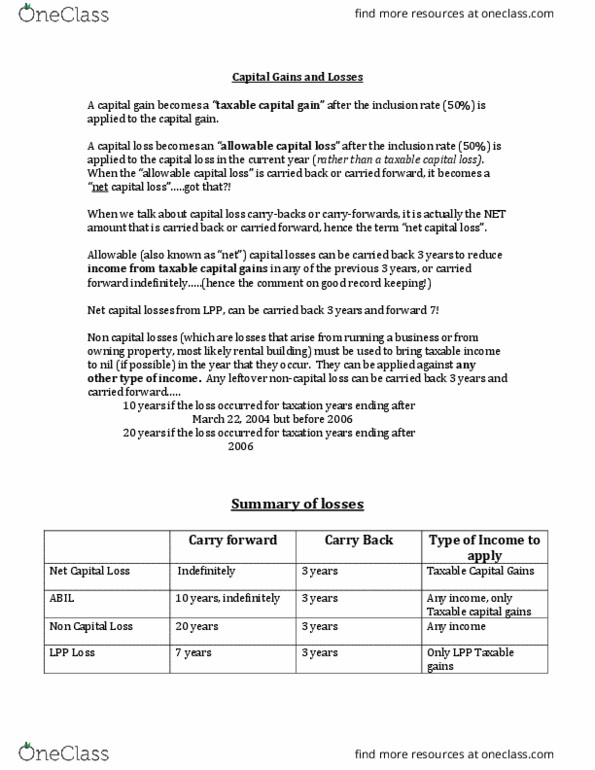

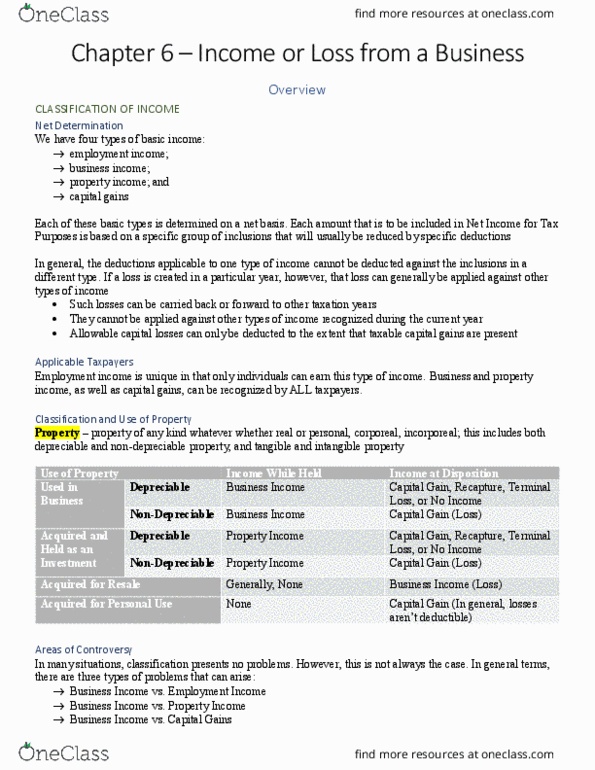

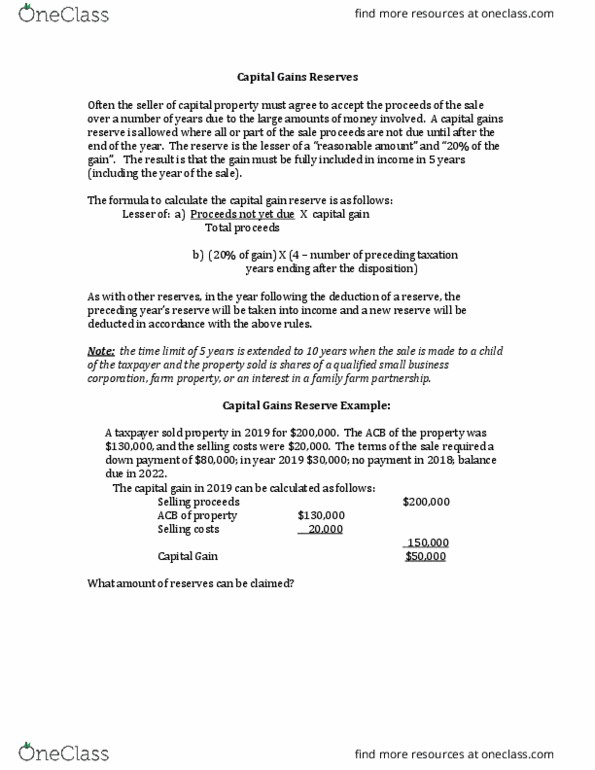

ACCT-4021EL Chapter Notes - Chapter 8: Capital Asset, Property Income, Capital Cost Allowance

Document Summary

Chapter 8 capital gains and capital losses. Capital gains and losses result from the disposition of assets that are being, or have been, used to produce business or property income. Regardless of favourable taxation, there was a continuing view that any taxation of such income was not appropriate. Therefore, in 1985, the government introduced the lifetime capital gains deduction. As of 2018, a lifetime deduction is available for the: Taxable part of an ,252 capital gain resulting from the disposition of shared of a qualified small business corporation. Taxable part of a ,000,000 capital gain on the disposition of qualified farming or fishing property. Qualified small business corporation a ccpc that uses substantially all (90% or more) of its assets to earn active business income in canada; taxpayer must have owned the shares for 2 years prior to sale & during those.