COMM-1106EL Chapter Notes - Chapter 3: Book Value, Trial Balance, Retained Earnings

6 Dec 2016

School

Department

Course

Professor

Document Summary

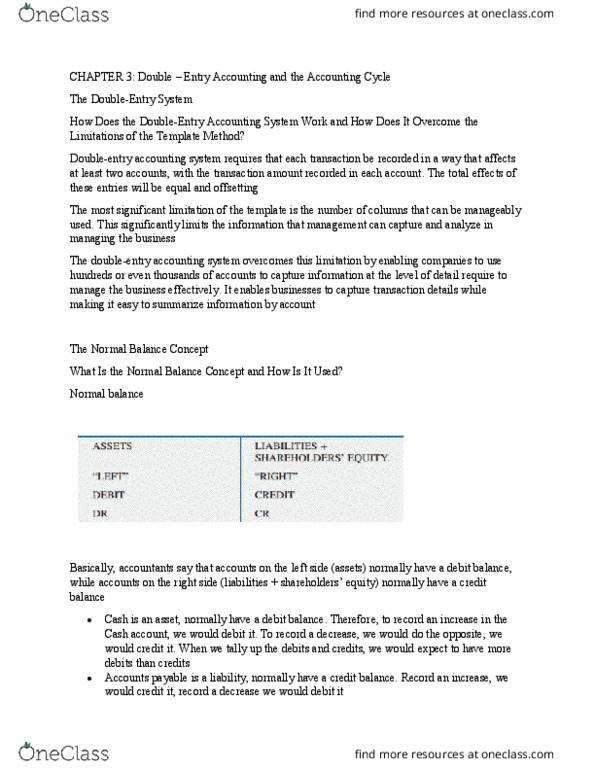

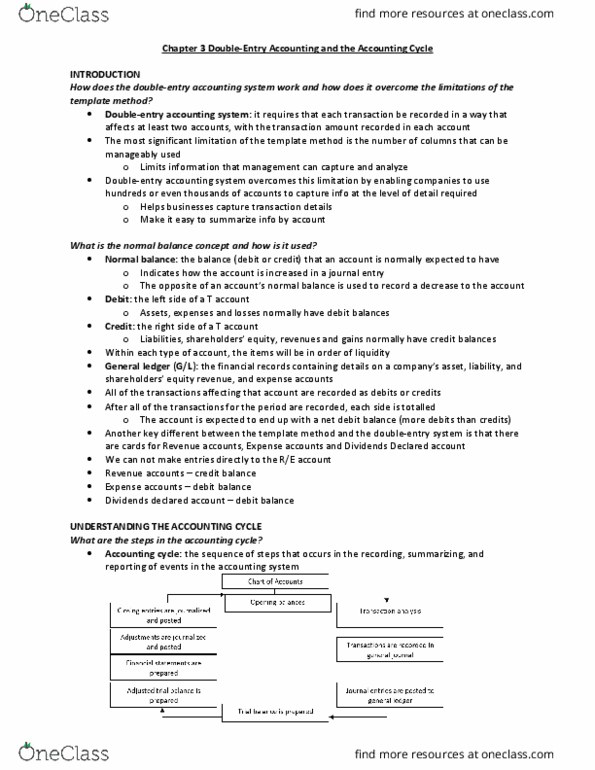

Chapter 3 dou(cid:271)le entry a(cid:272)(cid:272)ounting and the. Double entry accounting system: requires each transaction be recorded in a way that affect at least 2 accounts, with the transaction amount recorded in each account (in other words, the transaction amount is recorded twice, hence the term double ) The total effects of these entries will be equal and offsetting, similar to what we did in the template method, which required that each line balance. The most significant limitation of the template method is the number of columns that can be manageably used. This significantly limits the information that management can capture and analyze in managing the business, such as breaking down inventory separately, etc. The double entry accounting system overcomes this limitation by enabling companies to use hundreds or even thousands of accounts to capture information at the level of detail required to manage the business effectively.