COMM-2016EL Chapter Notes - Chapter 2: Unit, Longrun, Lincoln Near-Earth Asteroid Research

8 Sep 2017

School

Department

Course

Professor

Document Summary

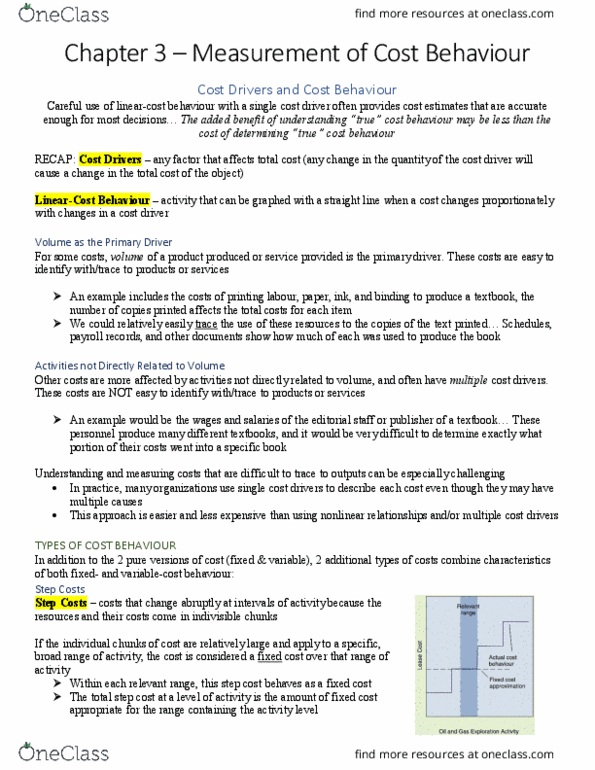

Chapter 2 cost behaviour a(cid:374)d cost volu(cid:373)e. Answering this question is the first step in analyzing cost behaviour . Cost behaviour how the activities of an organization affect its costs: a knowledge of patterns & cost behaviour offers valuable insights in planning & controlling operations. Cost drivers activities that affect costs: an organization has many cost drivers across its value chain, how well the accountant does at identifying he most appropriate cost drivers determines how well. Cost drivers managers understand cost behaviour and how well costs are controlled. Costs are classified as variable or fixed depending on how much they change as the level of a particular cost driver changes . Variable cost a cost that changes in direct proportion to changes in the cost driver (example: door-to-door salesman is paid 40% commission on their sales. Thus, sales commissions is a variable cost with respect to sales revenues)