COMM-2026EL Chapter Notes - Chapter 13: Capital Asset Pricing Model, Standard Deviation, Linear Combination

5 Dec 2017

School

Department

Course

Professor

Document Summary

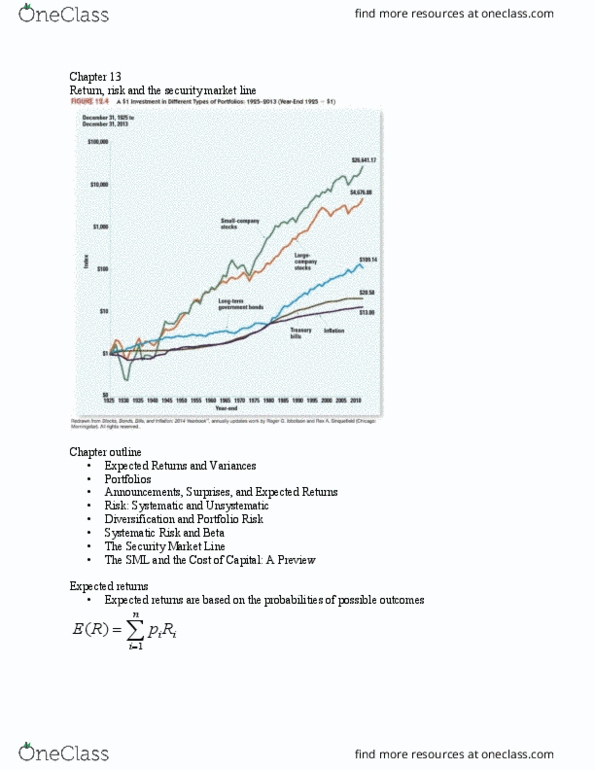

Chapter 13 return, risk, and the security market line. Expected return the return on a risky asset expected in the future (cid:1831)(cid:4666)(cid:1844)(cid:4667)= (cid:1844)(cid:3037)(cid:1876) (cid:3037) (cid:1831)(cid:4666)(cid:1844)(cid:4667) = expected return (cid:1844)(cid:3037) = value of the jth outcome (cid:3037)= the associated probability of occurrence. Suppose we think a boom and a recession are equally likely to happen if there is a recession, stock l will earn -20% and stock u will earn 30%. If there is a boom, stock l will earn 70% and stock u will earn 10%. If you hold stock u for several years, you will earn 30% half the time and 10% the other half. Expected risk premium = expected return e(r) risk-free rate (rf) Given this, what is the projected risk premium on. Since the expected return on stock u is 20%, the projected risk premium is: Risk premium = 0. 20 0. 08 = 12% Calculating the variance (cid:1848)(cid:1866)(cid:1855)(cid:1857)= 2= [(cid:4666)(cid:1844)(cid:3037) (cid:1831)(cid:4666)(cid:1844)(cid:4667)(cid:4667) 2 (cid:1876) (cid:3037)] (cid:1845)(cid:1866)(cid:1856)(cid:1856) (cid:1830)(cid:1857)(cid:1874)(cid:1867)(cid:1866)= = 2.