COMMERCE 1AA3 Chapter Notes - Chapter 9: Contingent Liability, Harmonized Sales Tax, Accrual

28 Nov 2016

School

Department

Course

Professor

Document Summary

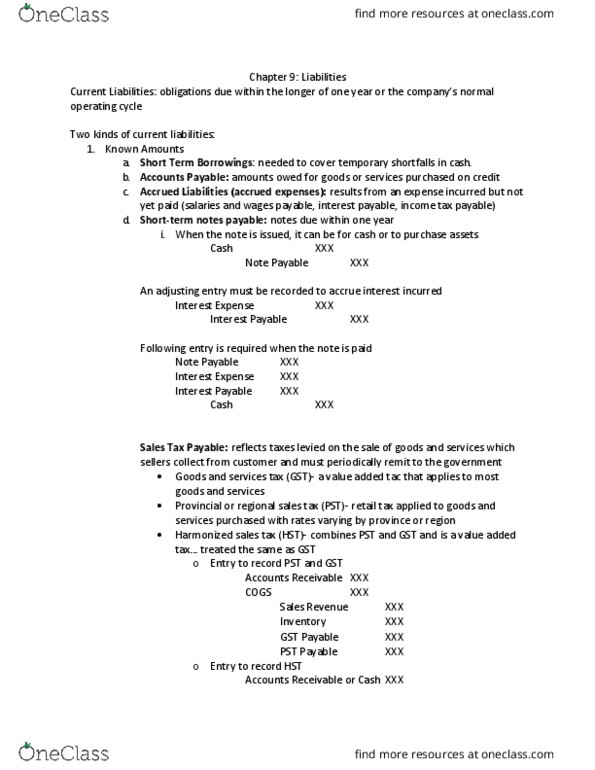

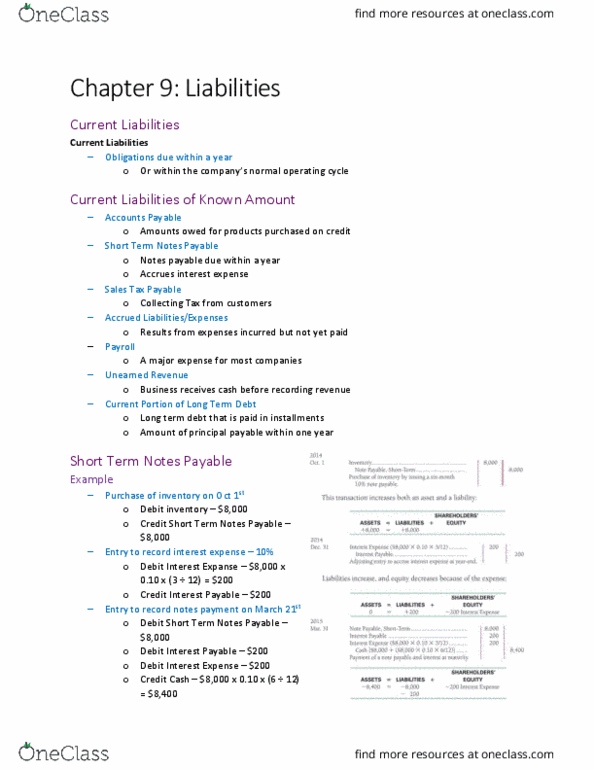

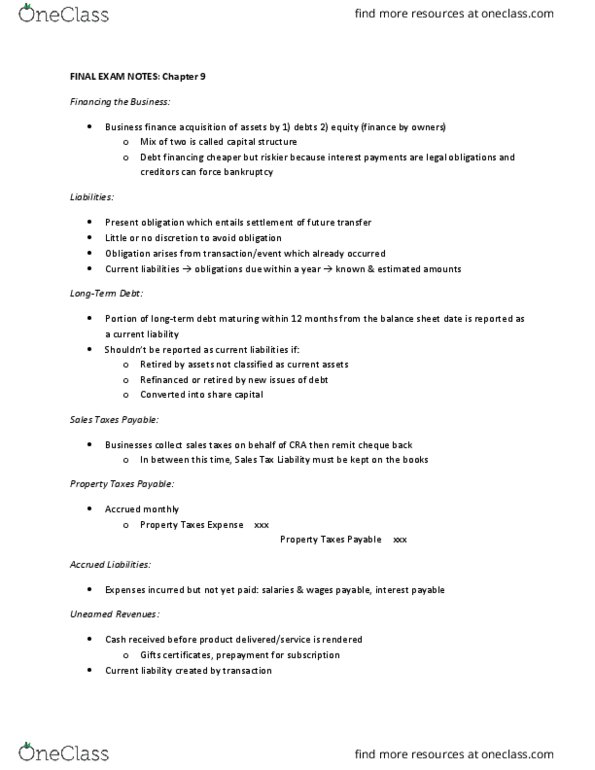

Learning objective one: explain and account for current liabilities. Current liabilities are obligations due within one year, or within the company"s normal operating cycle, if it is longer than one year. Obligations that are due beyond are classified as long-term liabilities. Two types of current liabilities: known amounts, estimated amounts. Companies sometimes need to borrow money on a short term basis to cover temporary shortfalls in cash needed to run their business. A line of credit allows a company to access credit on an as-needed basis up to a maximum amount set up by the lender. Amounts owed for products or services purchased on credit are accounts payable. An accrued liability results from an expense the business has incurred but has not yet been billed for or paid for. Common types of accrued liabilities: salaries and wages payable. The liability for salaries, wages, and related payroll expenses not yet paid at the end of the period.