COMMERCE 1AA3 Chapter Notes - Chapter 6: Round-Off Error, Perpetual Inventory, Weighted Arithmetic Mean

6 Dec 2016

School

Department

Course

Professor

Document Summary

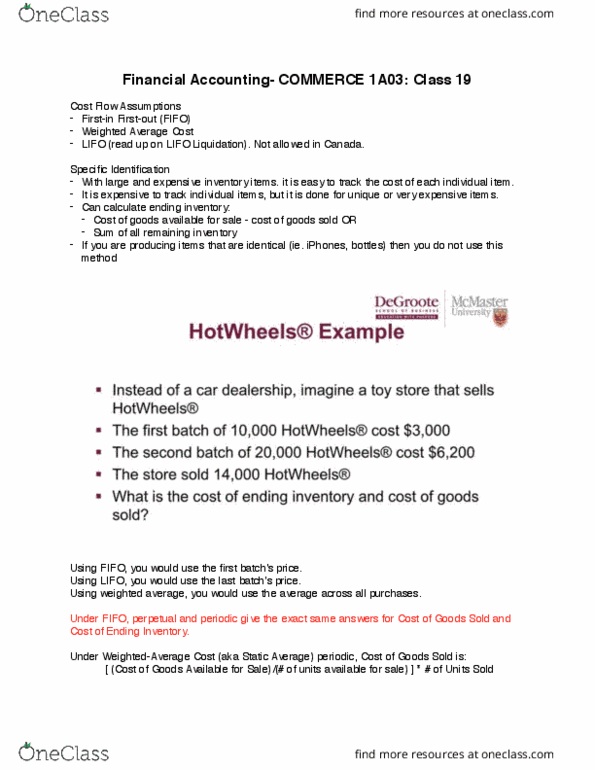

Once inventory quantity is determined, the second step is to measure its costs. Ideally, the cost of each unit is available and the cost of inventory is the sum of the costs of all units. In that case, specific identification is applied to cost inventory. This method tracks the specific items sold and on hand. The specific item prices are traced to purchase invoices. Special coding (such as bar codes) facilitates the use of this method. However, this method is impractical when large numbers of similar items are stocked. It is usually used for high cost items whose features tend to vary rather significantly. Car dealerships and jewelry stores commonly use this method. Sometimes it is difficult to obtain the costs of individual units if these units are purchased at different prices, and assumptions must be made about their costs. The cost assumptions generally used in practice are: first-in, first-out (fifo), weighted average cost, and.