COMMERCE 1AA3 Chapter Notes - Chapter 6: Inventory Turnover, Fifo (Computing And Electronics), Gross Margin

9 Jul 2017

School

Department

Course

Professor

Document Summary

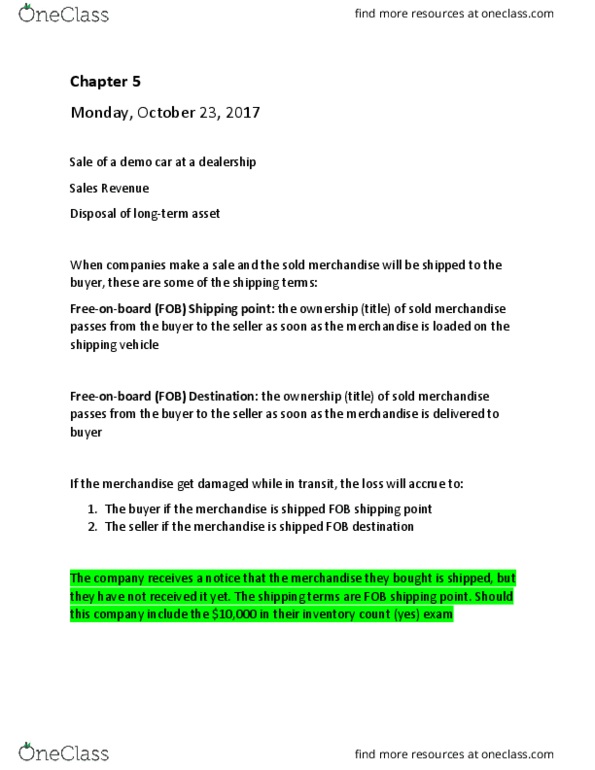

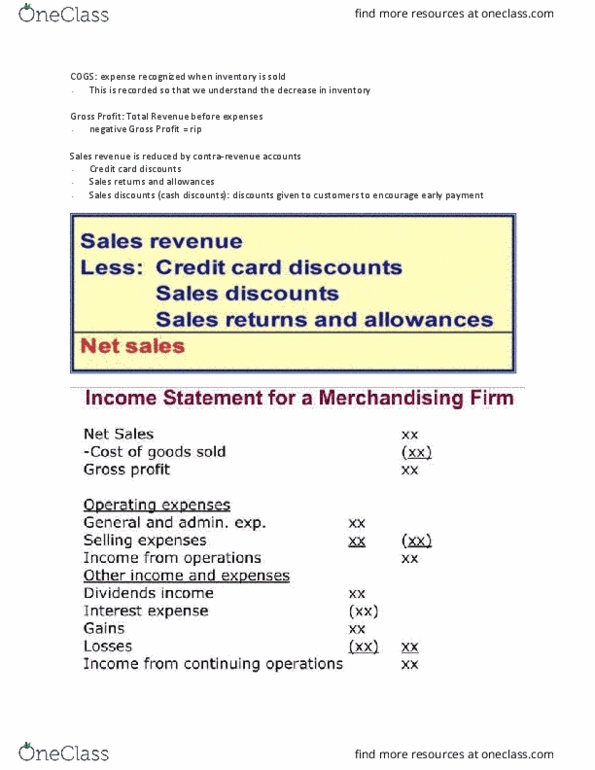

Perpetual inventory system: maintains a continuous record for each inventory item. Often used by a business that sells relatively fewer number of goods at a higher price per unit. Both purchases and sales of inventory are recorded directly to the inventory account. Qua(cid:374)tit(cid:455) a(cid:374)d (cid:272)ost of i(cid:374)(cid:448)e(cid:374)to(cid:396)(cid:455) (cid:272)a(cid:374) (cid:271)e dete(cid:396)(cid:373)i(cid:374)ed f(cid:396)o(cid:373) i(cid:374)(cid:448)e(cid:374)to(cid:396)(cid:455) (cid:396)e(cid:272)o(cid:396)ds a(cid:272)tual physical count must be made at least once a year. Perpetual records give up-to-the-minute data about inventory, enabling managers to make decisions about when and how much to buy. Two entries required to record sale of inventory: accounts receivable/cash, cost of goods sold. Periodic inventory system: does not keep a continuous record of the inventory on hand. Often used by businesses that sell a large number of goods at a low unit price. Purchases are recorded in the purchases account (an expense) Physical count of inventory is made at the end of period. Only one entry required to record sale of inventory: accounts receivable xxx.