COMMERCE 2AB3 Chapter Notes - Chapter 10: Budget, Income Statement, Fixed Cost

11 Apr 2017

School

Department

Course

Professor

Document Summary

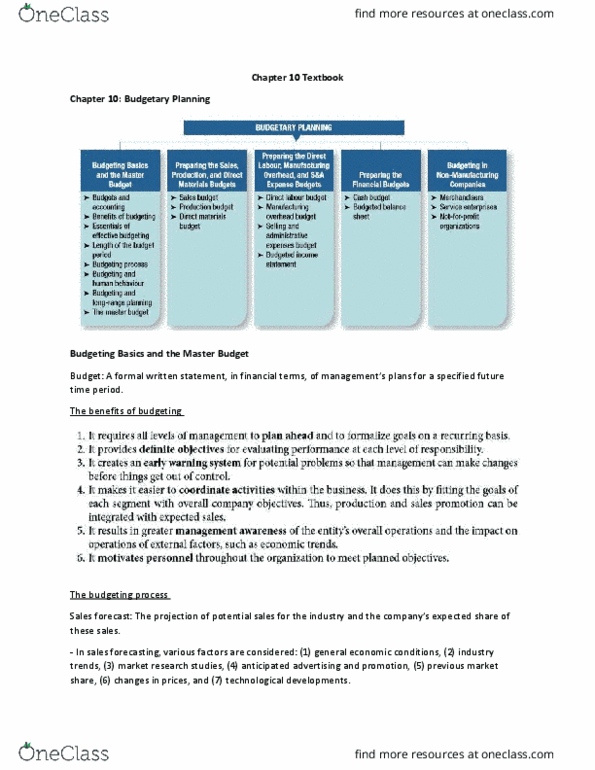

A formal written statement of management"s plans for a specified future time period, expressed in financial terms. Primary way to communicate agreed-upon objectives to all parts of the company. Control device- important basis for performance evaluation once adopted. Historical accounting data on revenues, costs, and expenses help in formulating future budgets. Accountants are normally responsible for presenting management"s budgeting goals in financial terms. The budget and its administration are, however, entirely management"s responsibility. Requires all levels of management to plan ahead and formalize goals on a recurring basis. Provides definite objectives for evaluating performance at each level of responsibility. Creates an early warning system for potential problems. Results in greater management awareness of he entity" overall operations and the impact of external factors. Motivates personnel throughout organization to meet planned objectives. A budget is an aid to management not a substitute for management. Depends on a sound organizational structure with authority and responsibility for all phases of operations clearly defined.