COMMERCE 2FA3 Chapter Notes -Net Present Value, Capital Budgeting, Capital Cost

30 Apr 2012

School

Department

Course

Professor

Document Summary

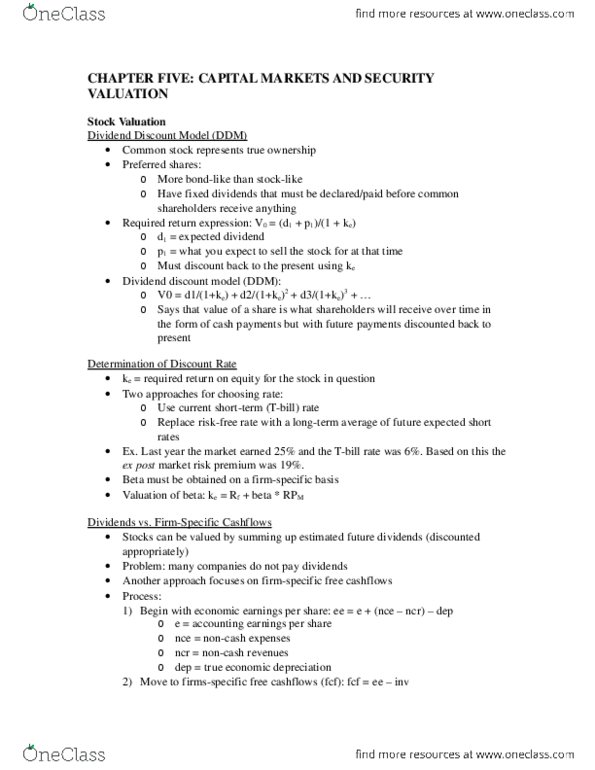

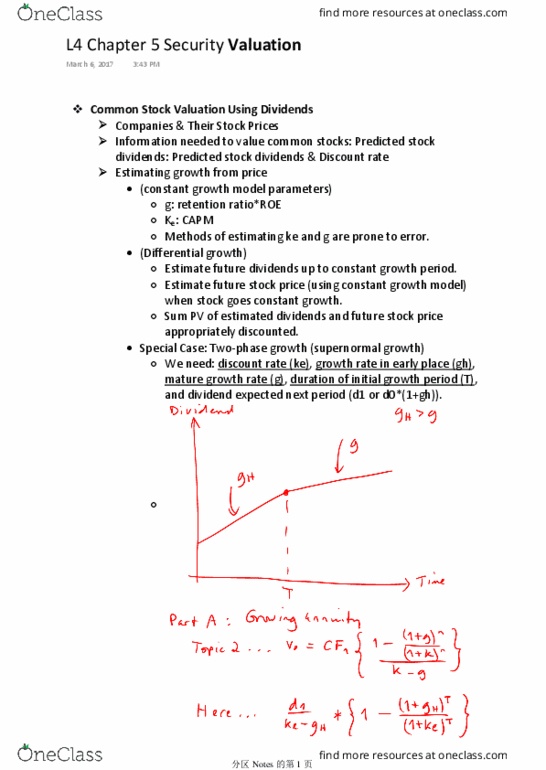

Let po be the current price of the stock, and define p1 to be the price in one period. If d1 is the cash dividend paid at the end of the period then, The dividend has a zero growth rate. Implies: d1 = d2 = d3 = d =constant. Value of the stock: po= d/(1+r)^n + . Since the dividend is always the same, the stock can be viewed as an ordinary perpetuity with a cash flow equal to d every period. The per-share value: po= d/r r- the required return: constant growth. If the dividend grows at a steady rate, g, the price can be written as: To avoid the problem of having to forecast and discount an infinite number of dividends, we require that the dividends start growing at a constant rate sometime in the future. Pt= dt x (1+g)/(r-g) t- number of periods.