COMMERCE 3FA3 Chapter Notes - Chapter 17: Dividend Policy, Dividend Tax, Dividend Yield

4 Dec 2017

School

Department

Course

Professor

Document Summary

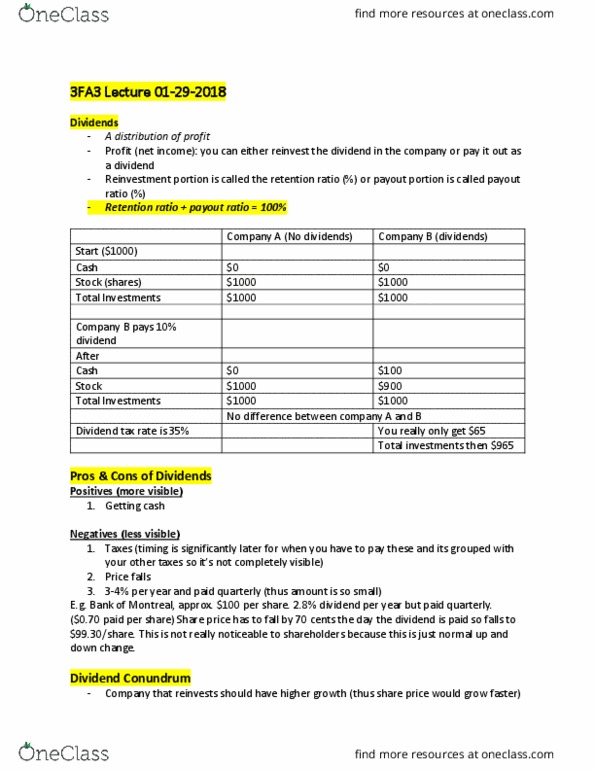

The hea(cid:396)t of the di(cid:448)ide(cid:374)d poli(cid:272)(cid:455) (cid:395)uestio(cid:374) is: (cid:862) should the fi(cid:396)(cid:373) pa(cid:455) out (cid:373)o(cid:374)e(cid:455) to sha(cid:396)eholde(cid:396)s o(cid:396) should the fi(cid:396)(cid:373) take that (cid:373)o(cid:374)e(cid:455) a(cid:374)d i(cid:374)(cid:448)est it fo(cid:396) its sha(cid:396)eholde(cid:396)s(cid:863) Distribution: if a payment is made from sources other than current or accumulated retained earnings. The most common type of a dividend is a regular cash dividend four times a year. A extra cash dividend implies it will not be repeated again in the future. A special dividend is similar but the name usually indicates that its viewed as unusual or one time event. A cash dividend payment reduced corporate cash and retained earnings, except in the case of a liquidating dividend (where capital may be reduced). Decisions to pay dividend by board of directors. When dividend declared it becomes a debt. The amount of cash dividend is expressed in dollars per share as, dividends per share.