ECON 1B03 Chapter Notes - Chapter 6-13: Free Trade, Price Floor, Comparative Advantage

8 Dec 2012

School

Department

Course

Professor

46

ECON 1B03 Full Course Notes

Verified Note

46 documents

Document Summary

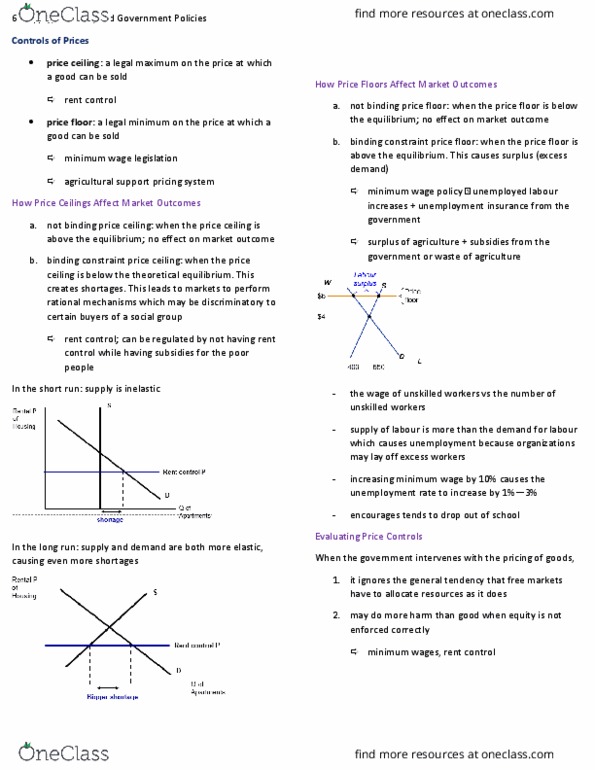

Price ceiling: a legal maximum on the price at which a good can be sold. Price floor: a legal minimum on the price at which a good can be sold. Not binding: if price ceiling is above equilibrium price, will not have effect on price or quantity sold because can still set price to what everyone is happy with. Binding constraint: if price ceiling is below equilibrium price, quantity demanded will exceed quantity supplied and there will be a shortage. Some buyers will get to buy at lower price, some will not get to buy at all. Causes long lines to develop and sellers to create personal biases about who they want to sell their goods to. Not binding: if price floor is below equilibrium price, has not effect on market forces or equilibrium. Binding constraint: if price floor is above equilibrium price, quantity supplied exceeds quantity demanded causing a surplus.