COMM 111 Chapter Notes - Chapter 6: Gross Margin, Income Statement, Financial Statement

Document Summary

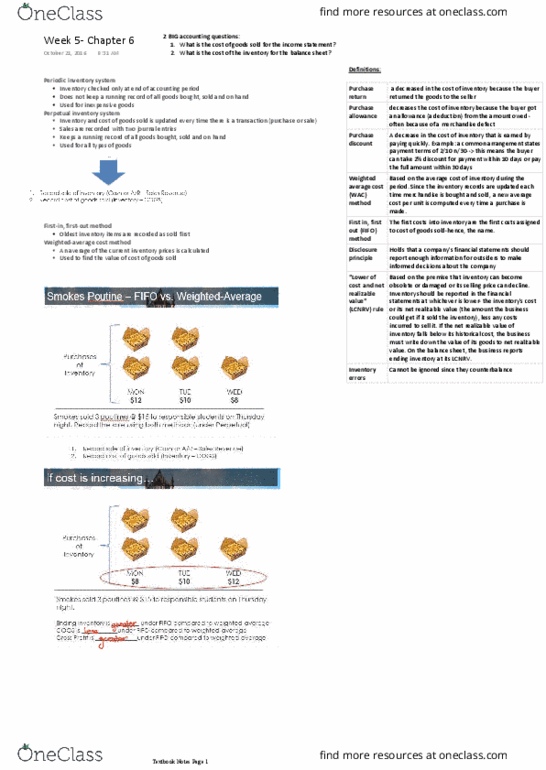

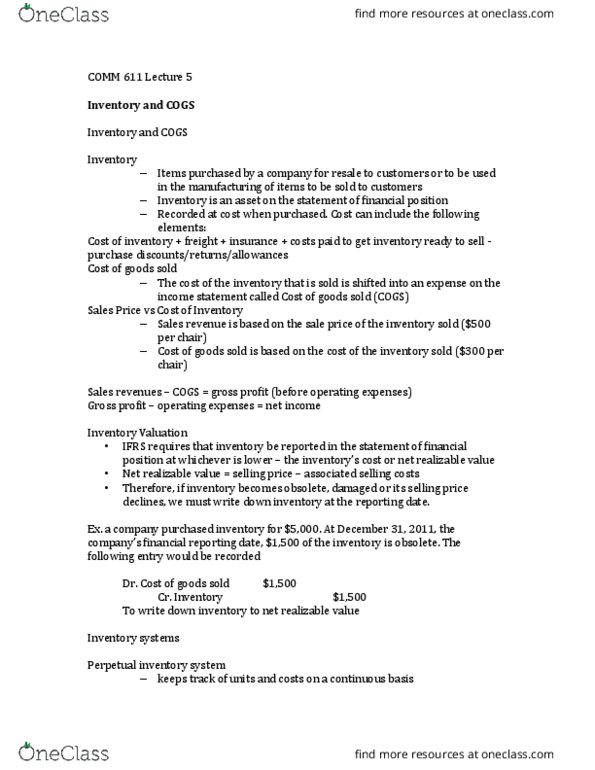

Chapter 6: inventory and cost of goods sold. Account for inventory using the perpetual and periodic inventory systems. Value of inventory affects two financial statements: inventory as an asset on the balance sheet, cogs as an expense on the income statement. Cost per unit of inventory: difficult because companies purchase goods at different prices throughout the year. Includes basic purchase price, plus freight in, insurance while in transit, and any costs paid to get inventory ready to sell, less returns, allowances and discounts. Periodic inventory system: mainly used by businesses that sell inexpensive goods, count inventory periodically (i. e once a year, used for inexpensive goods, does not keep a running record of all goods bought, sold and on hand. Recording transactions (perpetual: each purchase of inventory is recorded as a debit to inventory and credit to cash or accounts payable. Inventory costing methods: specific identification cost, weighted-average cost, first in, first out (fifo) cost.