ACC 100 Chapter Notes - Chapter 3: Deferral, Accounts Payable, Asset

4 Dec 2017

School

Department

Course

Professor

Document Summary

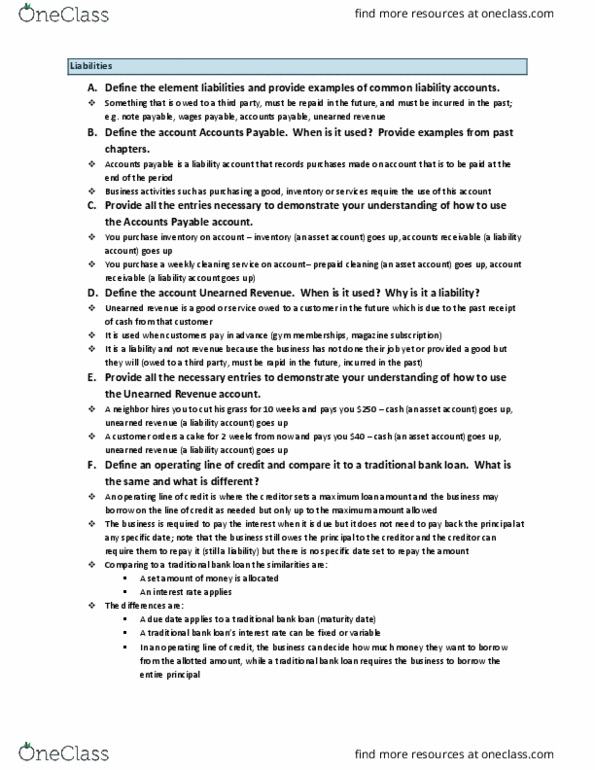

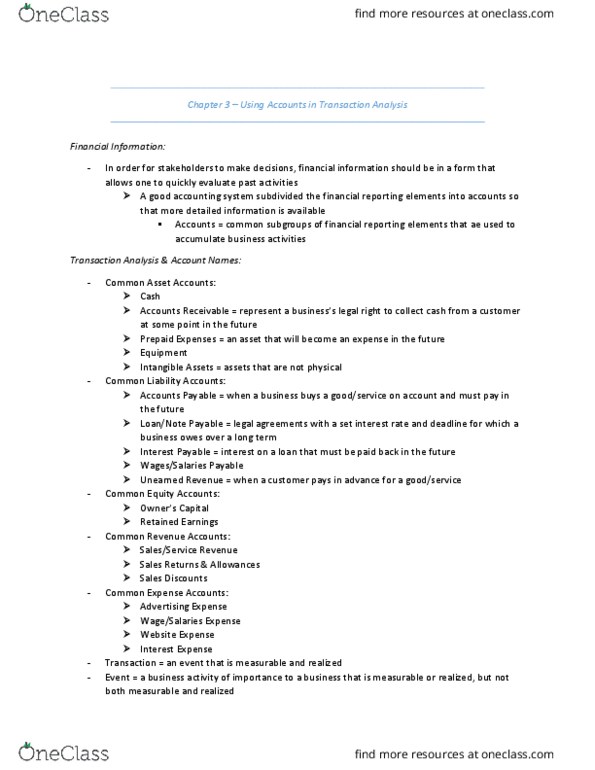

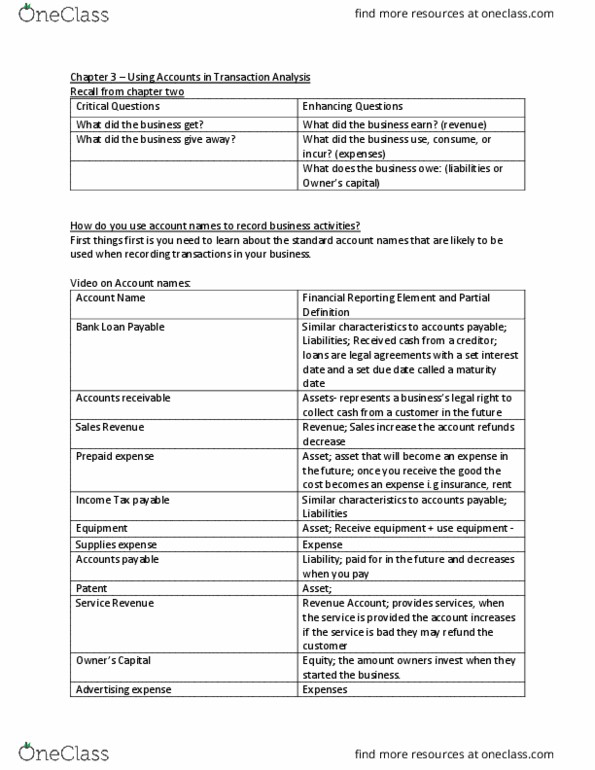

Introduction to accounts: recognize the difference between events and transactions. An event is a business activity of importance to a business, For something to be an event it must be either measureable but not realized, or realized but not measurable. Events are never recorded in the accounting system. For an even to be a transaction, it must be measurable and realized. Transactions are recorded in the accounting system: analyze and record transactions using the critical and enhancing questions, record all transactions using account names. Leasing of a domain name with a credit card prepaid expense (an asset account) goes up, accounts payable (a liability account) go up. Purchase of a business license on credit card business license (an asset account; more specifically a long- lived, tangible asset) goes up, accounts payable (a liability account) go up. Cash contributions by owners (cid:272)ash (cid:894)a(cid:374) asset a(cid:272)(cid:272)ou(cid:374)t(cid:895) goes up, o(cid:449)(cid:374)e(cid:396)"s (cid:272)apital (cid:894)a(cid:374) e(cid:395)uity a(cid:272)(cid:272)ou(cid:374)t(cid:895) goes up.