ACC 100 Chapter 4: ACC 100 Chapter 4 Notes.docx

13 Mar 2012

School

Department

Course

Professor

Document Summary

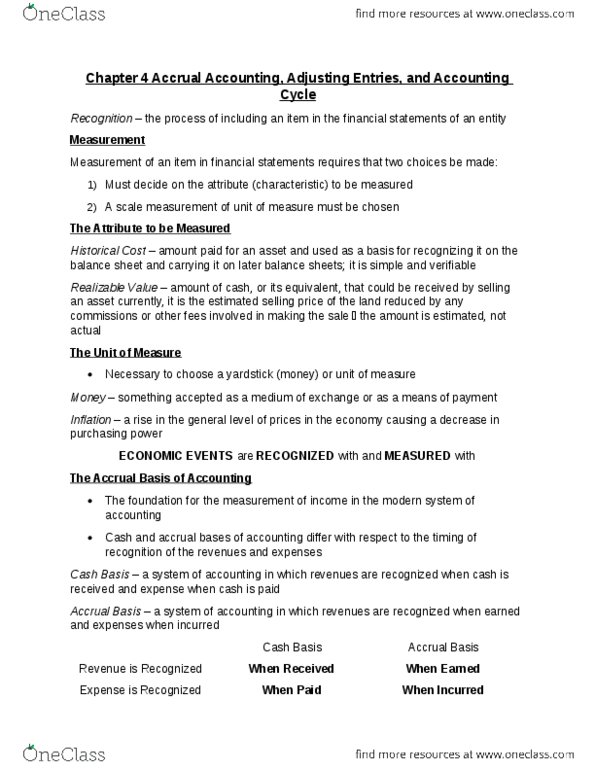

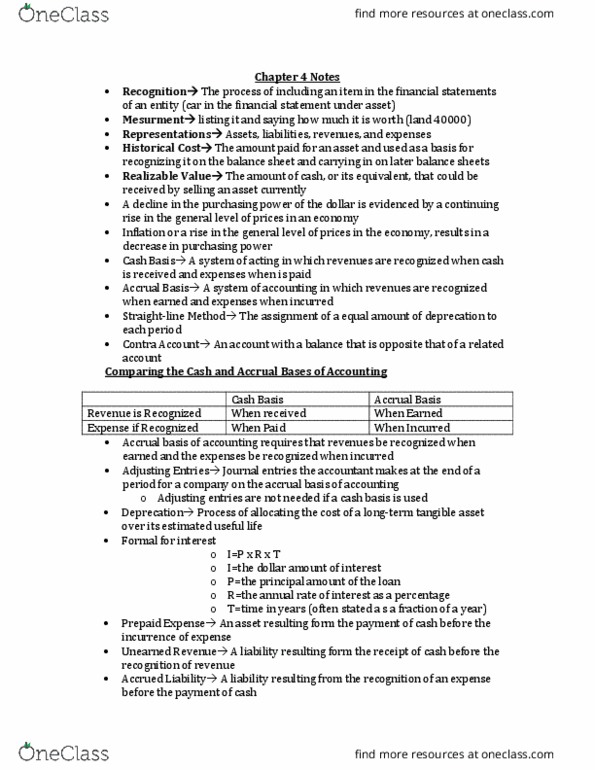

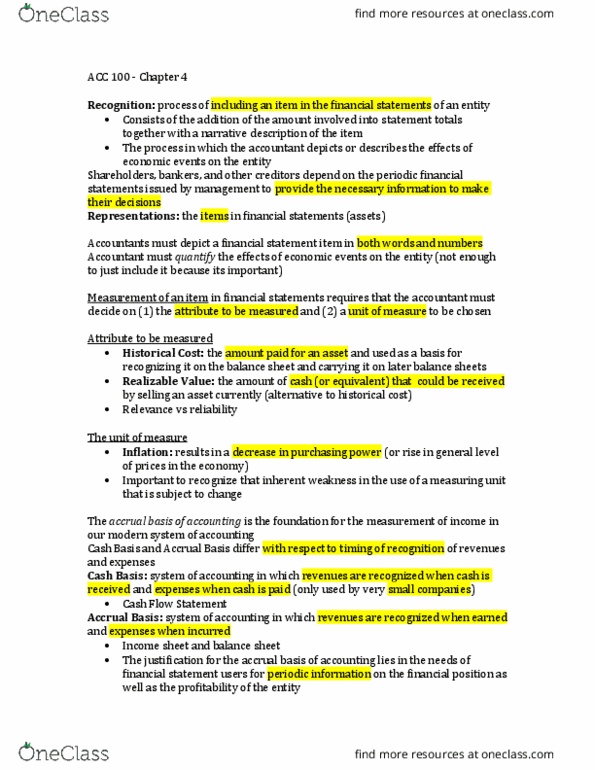

Recognition: the process of including an item in the financial statements of an entity. Measurement: the attribute to be measured. Historical cost: the amount paid for an asset and used as a basis for recognizing it on the balance sheet and carrying it on later balance sheets. Realizable value: the amount of cash, or its equivalent, that could be received by selling an asset currently: unit of measure. The yardstick we currently use is units of money. Money is something accepted as a medium of exchange or as a means of payment. Cash basis: a system of accounting in which revenues are recognized when cash is received and expenses when cash is paid. Accrual basis: a system of accounting in which revenues are recognized when earned and expenses when incurred. Adjusting entries: journal entries made at the end of a period by a company using the accrual basis of accounting.