ACC 406 Chapter Notes - Chapter 9: Cash Flow, Income Statement, Longrun

2 Apr 2017

School

Department

Course

Professor

Document Summary

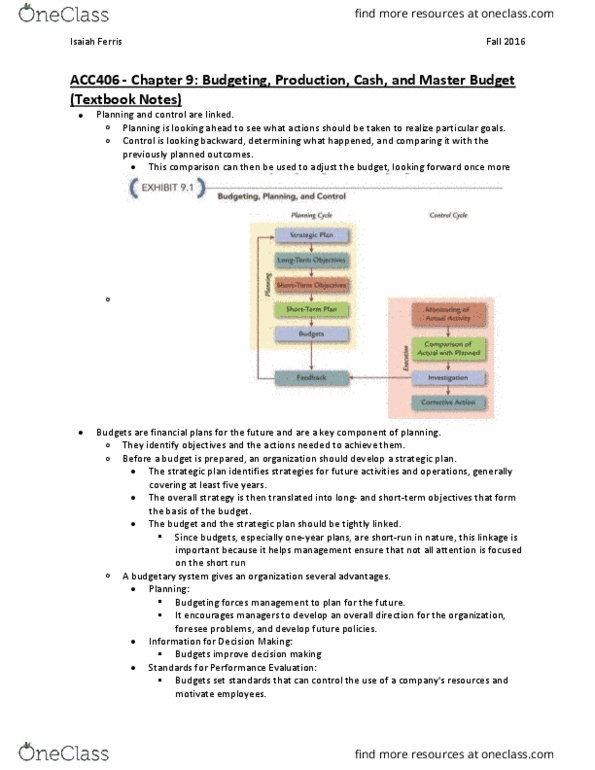

Budgets help business owners and managers to plan ahead, and later, exercise control by comparing what actually happened to what was expected according to the budget. Planning is looking ahead to see what actions should be taken to realize particular goals. Control is looking backward, determining what actually happened, and comparing it with the previously planned outcomes. Budgets are financial plans for the future and are a key component of planning. Before one is planned, a firm should develop a strategic plan, which identifies strategies for future activities and operations, generally covering at least 5 years. The overall strategy is then translated into long- and short-term objectives. Planning budgeting force management to plan for the future and develop a direction. Information for decision making budgets improve decision making. Standards for performance evaluation budgets set standards that can control the use of a company"s resources and motivate employee.