ACC 406 Chapter Notes - Chapter 1: Management Accounting, Finished Good, Variable Cost

13 Sep 2012

School

Department

Course

Professor

Document Summary

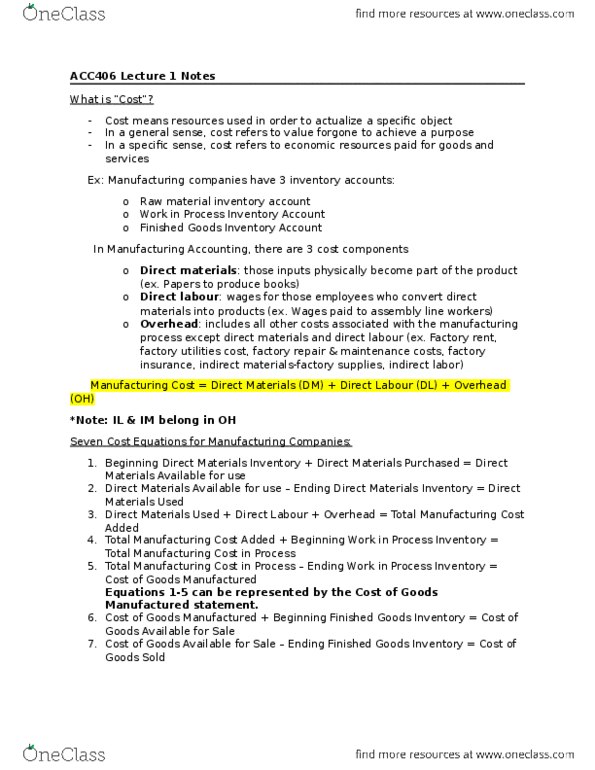

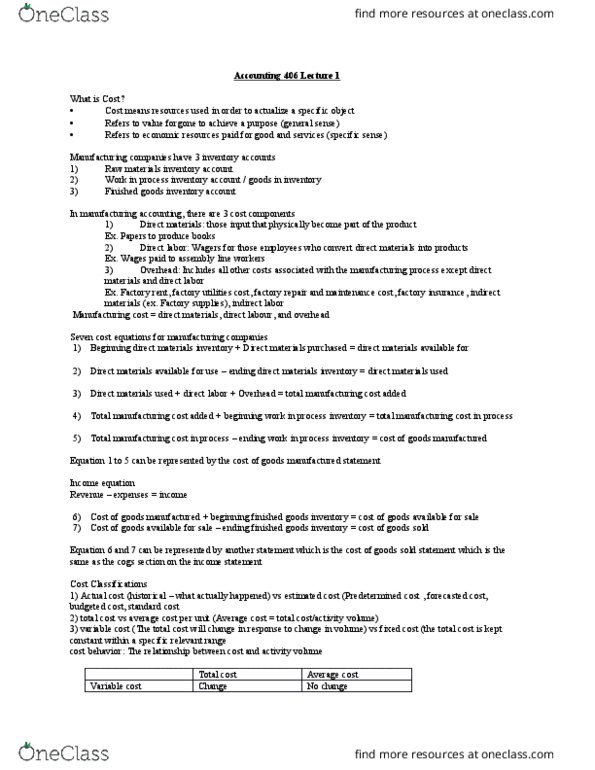

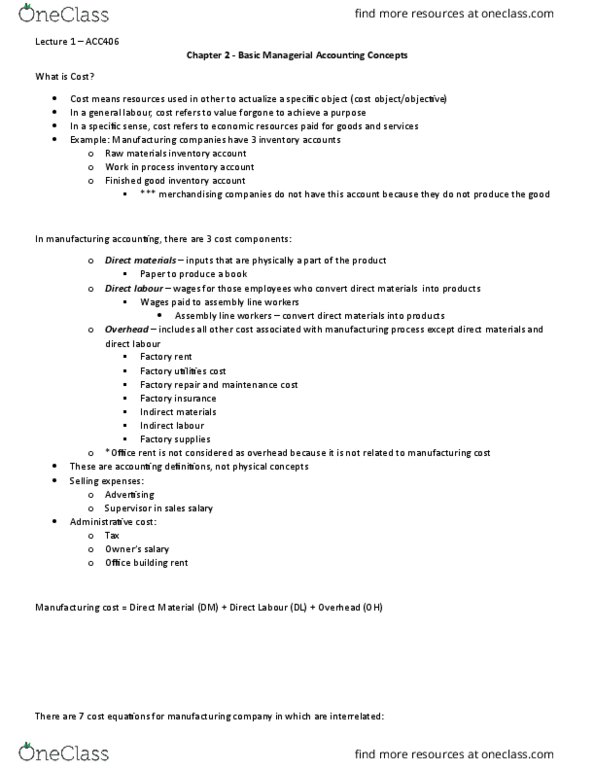

Cost means resources used to actualize a specific object (cost objective) In general, cost refers to value forgone to achieve a purpose. In specific, cost refers to economics resources paid for goods and services. Manufacturing companies have 3 inventory accounts: raw material inventory account, work in process inventory account, finished goods inventory account. In manufacturing accounting, there are 3 cost components: direct materials. These inputs physically become part of the product. Wages paid for those employees who convert direct materials into product. Wages paid to assembly line workers: overhead: includes all other cost associated with the process (except for direct loss. Factory rent, factory utilities repair and maintenance, insurance, indirect materials, indirect labour. Equation 1-5 can be represented by the cost of good manufactured statement. Equation 6-7 can be represented in cost of goods sold section on the income statement. Cost of goods sold: actual cost versus estimated cost.