ACC 410 Chapter 3: Chapter 3

15 Apr 2011

School

Department

Course

Professor

Document Summary

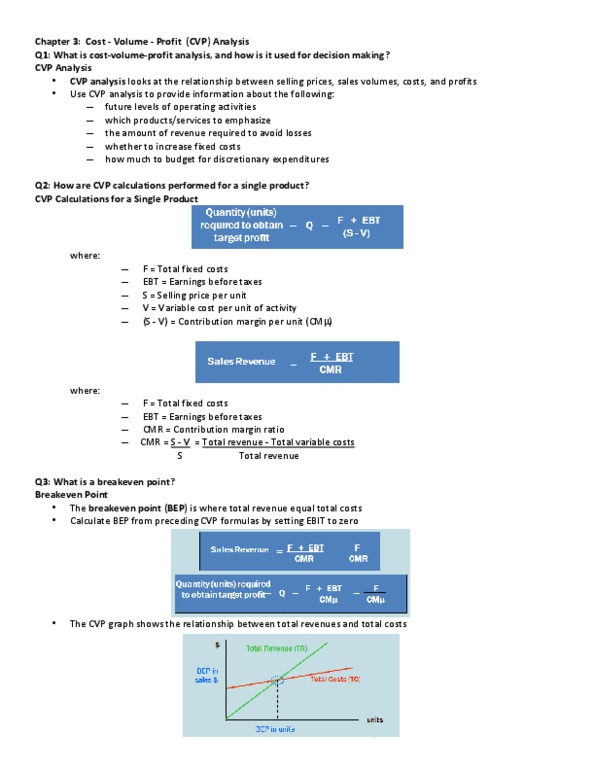

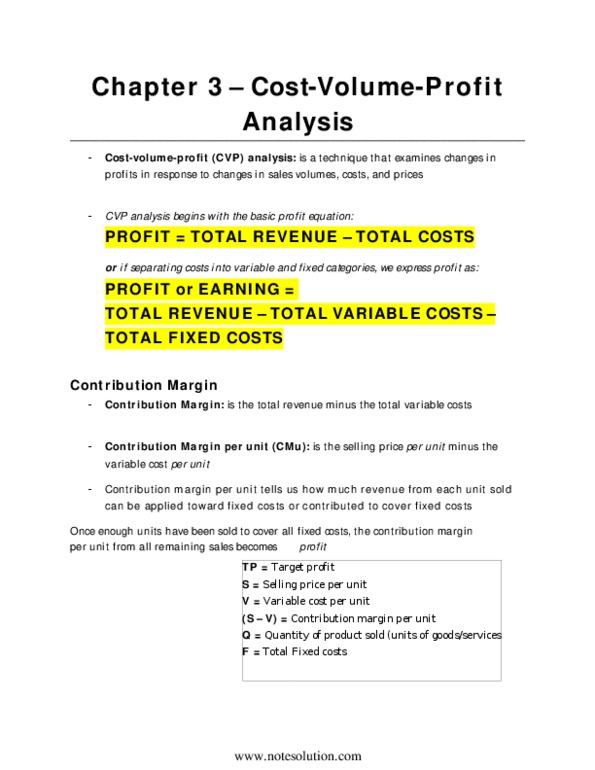

cost- volume- profit (cvp) analysis: technique that examines changes in profits in response to changes in sales volume, costs, and prices. cvp describes volume, revenues, costs and profits and plan future level of operating activities. values at breakeven or target profit units sold revenues variable, fixed, and total costs. sensitivity of results to changes in: levels of activity cost function selling price sales mix indifference point between alternatives feasibility of planned operations. contribution margin (cm): total revenue minus total cost. profit = total revenue total cost. cm = total revenue total variable cost. cmu (per unit) = selling price per unit variable cost per unit. cmr = s v / s. ebt ( earnings before taxes) = (s-v) x q f. eat (earnings after taxes) = ebt x (1 tax rate) ebt = eat / (1 tax rate) operating income = sales vc fc.