ACC 410 Chapter 2: chapter 2 notes

14 May 2011

School

Department

Course

Professor

Document Summary

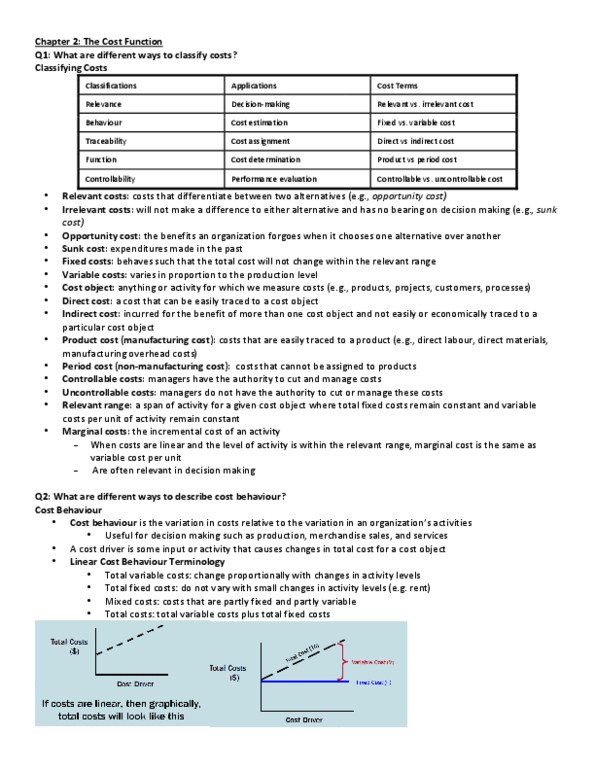

Managers who understand how costs behave are better able to predict costs and make decisions under various circumstances. This chapter explores the meaning of three major classifications of costs fixed, variable and mixed costs various methods available to estimate fixed and variable cost components. Types of cost behaviour patterns at least three types of cost behaviour patterns variable, fixed, and mixed are found in most organizations. There are many other types of cost behaviour patterns but these three patterns are fairly common and the mixed cost model can be used to provide approximations to more complex cost behaviour patterns within a relevant range. It is important for managers to understand the behaviour of each type of cost: variable costs. A variable cost is one whose total dollar amount varies in direct proportion to changes in the activity level. When expressed on a per unit basis, variable costs are constant: activity base (cost driver).