ACC 110 Chapter Notes - Chapter 3: Deferral, Deferred Income, Profit Margin

1 May 2012

School

Department

Course

Professor

Document Summary

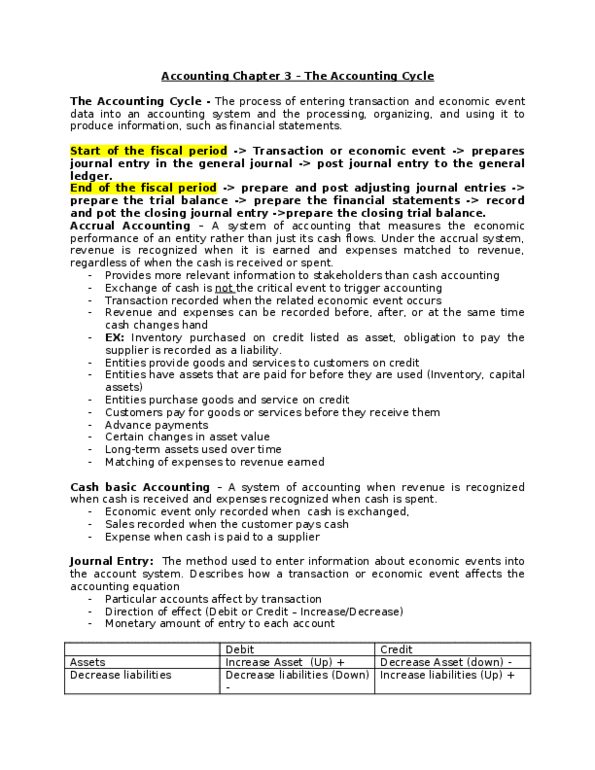

The accounting cycle is the process of entering transaction and economic event data into an accounting system and then processing, organizing, and using it to produce information, such as financial statements. Panel a, provides an overview of an accounting system"s role in capturing raw data, processing it, and producing financial statements and other financial information. An accounting system is designed to capture relevant economic events affecting the entity. A relevant event must be entered into the accounting system in some way it does not happen automatically and judgment is required to decide if, when, and how the event is recorded. Accrual accounting: accrual accounting provides more relevant information to stakeholders than cash accounting does. Cash doesn"t have to be exchanged when an economic event is recorded: accrual accounting: inventory purchased on credit is recorded as an asset, and the obligation to pay the supplier is recorded as a liability.