FIN 300 Chapter Notes - Chapter 2: Operating Cash Flow, Fixed Asset, Cash Flow

16 Oct 2011

School

Department

Course

Professor

Document Summary

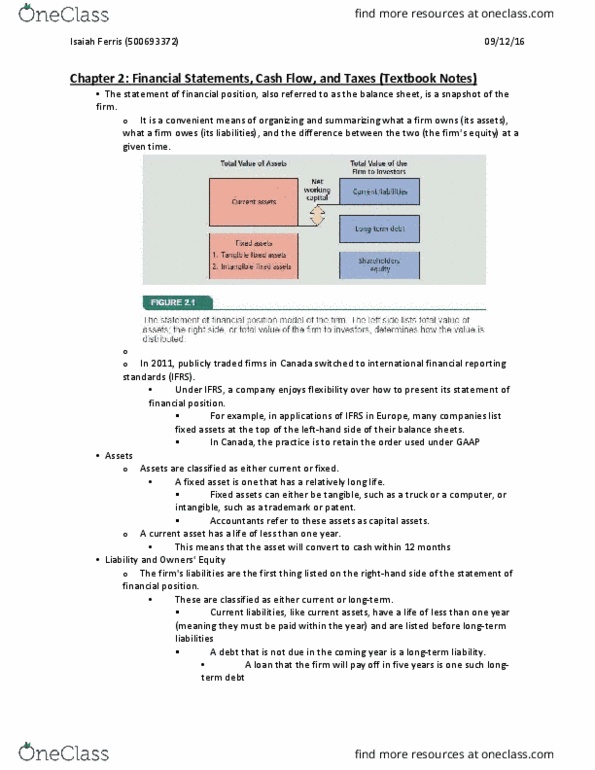

It is a convenient means of organizing and summarizing what a firm owns( its assets), what a firm owes ( its liabilities), and the difference between the two ( the firm"s equity) at a given time. A fixed asset is one that has a relatively long life. Accountants refer to these assets as capital assets. Current assets have a life of less than one year. Liabilities and owners equity: the right hand side. Current liabilities have a life of less than one year. Bond and bondholders refer to long term debt and long term creditors. The difference between the total value of the assets (current and fixed) and the total value of the liabilities (current and long term) is the shareholders equity aka common equity or owners equity. Difference between a firms current assets and its current liabilities is called net working capital.