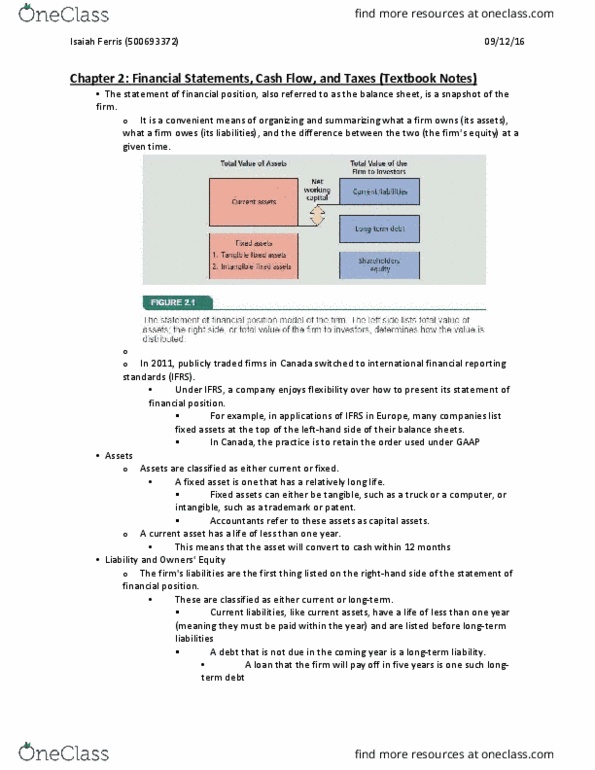

Using the 2005 and 2006 Statement of Financial Position (SFP) and the Statement of Earnings (SE) found on pages 465 and 466, complete a vertical analysis (common-sized statements) for both years and a horizontal analysis (trend) from 2005 to 2006.Please show work.......thanks

Table13:1

Bayside Memorial Hospital Statements of Operations (Income Statements) Years Ended December 31, 2006 and 2005 (Thousands of dollars 2006 2005

Net Patient Service Revenue $108,600 $97,393

Premium revenue 5,232 4,622

Other revenue $ 3,644 6,014

Total revenues $117,476 $108,029

Expense:

Nursing Services $58,245 56,752

Dietary Services 5,424 4,718

General services 13,198 11,655

Administrative services 11,427 11,585

Employee health and welfare 10,250 10,705

Provision for uncollectible 3,328 3,469

Provision for malpractice 1,320 1,204

Depreciation 4,130 4,025

Interest expense 1,542 1,521

Total Expense $108,904 $105,634

Net Income $8,572 $2,395

Balance Sheet

Table 13.2 contains Bay sideâs 2005 and 2006 balance sheets. Although the assets are all stated in terms of dollars, only cash represents actual money we see that bayside can if it liquidated its short-term investment securities. Write checks at the end of 2006 for a total $6,263,000 (verse total current liabilities of $13,332,000 due during 2006). The noncash current assets will presumably be converted to cash within a year, but they do not represent cash on hand.

Then Claims against assets are two types: 1) liabilities, or money the firm owes, and 2) equity, also called net assets or fund capital. Equity is a residual, so for 2006

Assets -Liabilities = Equity

151,278,000 - ($13,332,000+$30,582,000) =$107,364,000

Liabilities consist of $(13,332,000 of current liabilities plus $30,582,000of long-term liabilities. If assets decline in value-suppose some of Baysideâ s fixed assets were sold at less that book value-liabilities remain constant, so the value of the equity capital declines.

Table 13:2 Bayside Memorial Hospital Balance Sheets December 31, 2006 and 2005 (thousand of dollars)

2006 2005

Cash $4,263 $5,095

Short-term investments 2,000 0

Accounts receivable 21,840 20,738

Inventories 3,177 2,982

Total current assets $31,280 $28,815

Gross plant and equipment $145,168 $140,865

Accumulated depreciations 25,160 21,030

Net plant and equipment $119,998 $119,835

Total assets $151,278 $148,650

Accounts payable $4,707 $5,145

Accrued expenses 5,650 5,421

Notes payable 825 4,237

Current portion of long-term debt 2,150 2,000

Total current liabilities $13,332 $16,803

Long-term debt $28,750 $30,900

Capital lease obligations 1,832 2,155

Total long-term liabilities $30,582 $33,055

Net assets (equity) $107,364 $98,792

Total liabilities and net assets $151,278 $148,650