ECN 104 Chapter Notes - Chapter 13: Farmer Jack, Average Cost, Marginal Product

14 Nov 2011

School

Department

Course

Professor

Document Summary

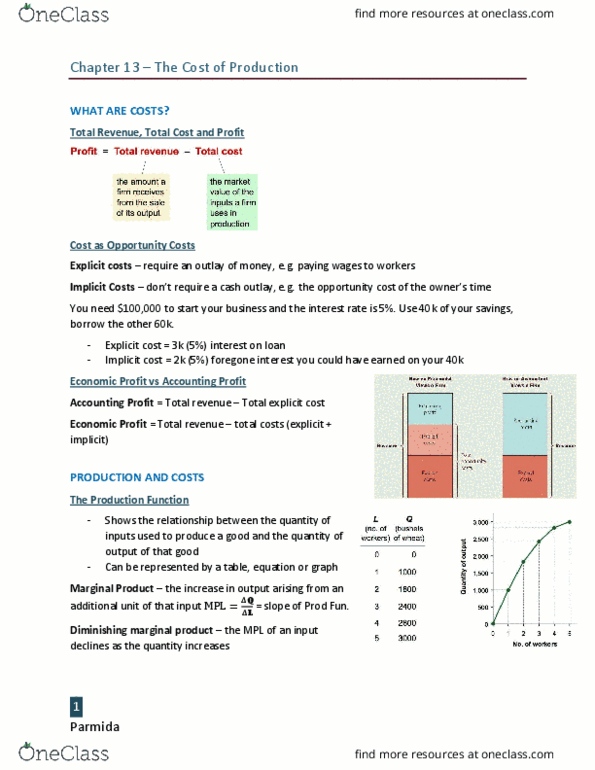

The cost of something is what you give up to get it firms" decisions. You need ,000 to start your business. Interest rate is 5: borrow ,000, explicit cost = interest on loan. Case 2: use ,000 of your savings, borrow the other ,000, explicit cost = (5%) interest on the loan. Implicit cost = (5%) foregone interest you could have earned on your ,000. His costs rise by the wage he pays the worker. His output rises by mpl: comparing them helps jack decide whether he would benefit from hiring the worker, why mpl diminishes additional worker. Fixed and variable costs: fixed costs (fc) do not vary with the quantity of output produced. For farmer jack, fc = for his land. Other examples: cost of equipment, loan payments, rent: variable costs (vc) vary with the quantity produced. For farmer jack, vc = wages he pays workers.