FIN 300 Chapter Notes - Chapter 7: Hybrid Security, Nominal Interest Rate, Convertible Bond

Document Summary

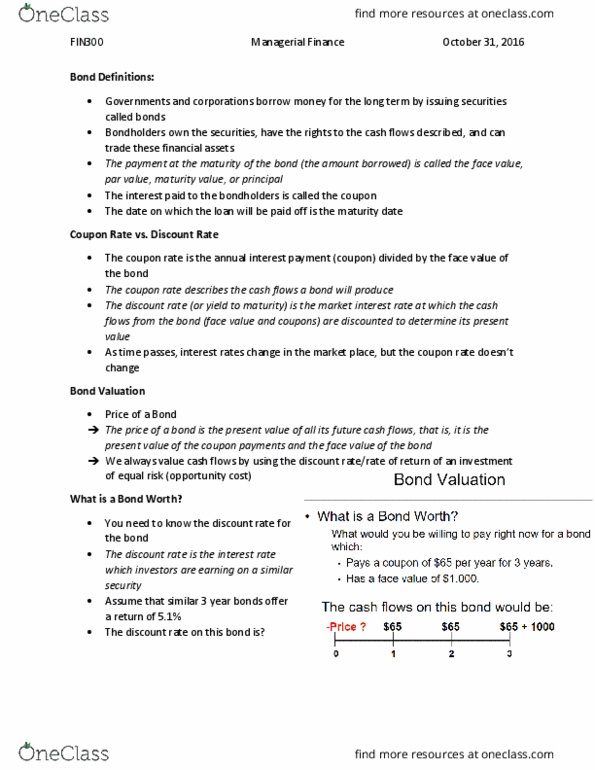

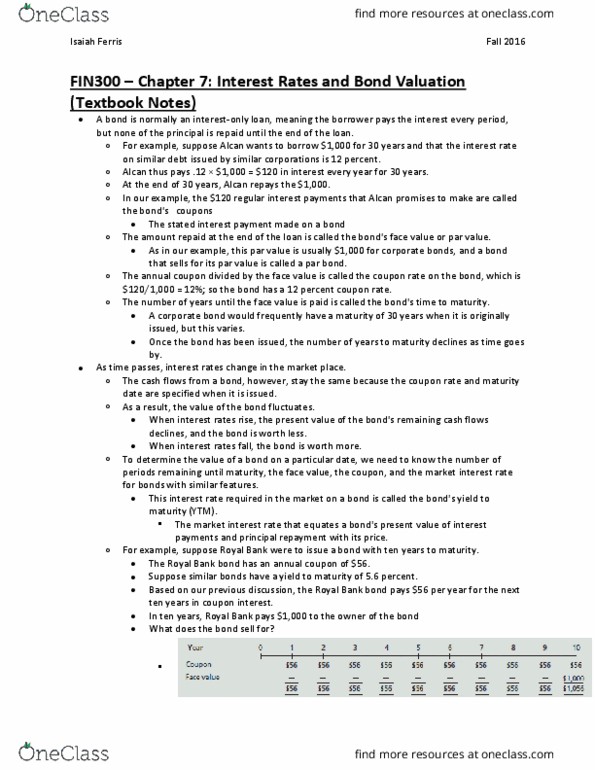

Fin 300 chapter 7: interest rates and bond valuation. When a corporation or a government wishes to borrow money from the public on a long-term basis, it usually does so by issuing or selling debt securities that are generically called bonds. Bond is normally an interest-only loan, meaning the borrower pays the interest every period, but none of the principal is repaid until the end of the loan. Coupons the stated interest payments made on a bond. If coupon is constant and paid every year, those types of bonds are called level coupon bond. Face value the principal amount of a bond hat is repaid at the end of the term. Coupon rate the annual coupon divided by the face value of a bond. Maturity date specified date at which the principal amount of a bond is paid: once a bond is issued, the number of years to maturity declines as time goes by.