FIN 512 Chapter Notes - Chapter 7: Unemployment Insurance Act 1920, Unemployment Benefits, Disability Insurance

17 Jul 2012

School

Department

Course

Professor

Document Summary

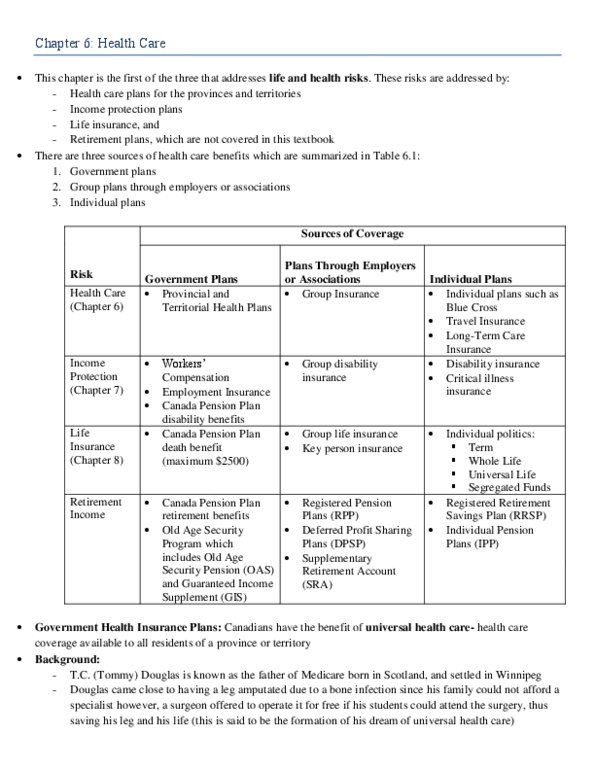

Income protection is crucial for most workers during times of job loss, illness, or sickness because when someone cannot work, in addition to losing income, there are frequently additional expenses. Group and individual plans can supplement government plans in those instances where government coverage is either not available or inadequate. Government plans: there are 3 government plans that offer income protection for workers who are not able to work due to the following: Ill health, which is covered by worker s compensation, employment insurance, and canada pension. Unemployment that is short-term and involuntary and is often covered by employment insurance. All of these government programs fall under the descriptor social insurance because their primary focus is to provide compulsory protection for personal risks. Other benefits also fall under this heading, such as canada pension plan, retirement benefits, and death benefits.