LAW 603 Chapter Notes - Chapter 14: Confidence Trick, Bearer Instrument, Promissory Note

8 Apr 2014

School

Department

Course

Professor

Document Summary

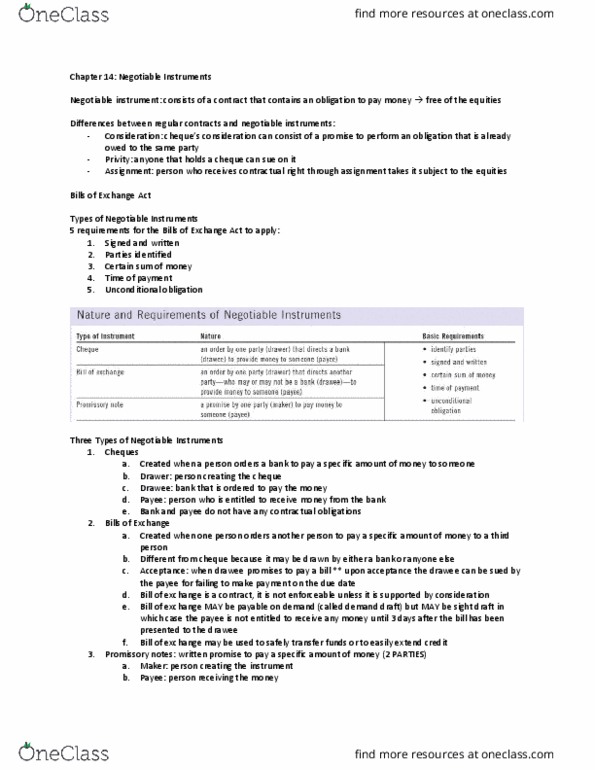

Chapter 14 special contracts: negotiable instruments (p 335) Lesson; don"t carry more cash than prepared to do without. Consists of contract that contains obligation to pay money: represents compromise between simple contract and money. Buy car from dealership contract; required to pay price dealer required to transfer car. Shouldn"t carry 000 cash with you; you write a cheque cheque is a new contract; promise that 000 will be in your bank. If bank refuses to honour cheque; dealer can so you on either sale contract or cheque. Important differences between negotiable instrument and contracts: consideration. Same: cheque must be supported by consideration; giving something of value in return. Normal rule; consideration can"t consist of promise to perform obligation that is already owed to same party but with cheque it can. Dealership"s promise to give car acted as consideration twice; for sale contract and for cheque: privity.