SOC 506 Chapter Notes -Fixed Cost, Variable Cost, Cost Accounting

25 Nov 2013

School

Department

Course

Professor

Document Summary

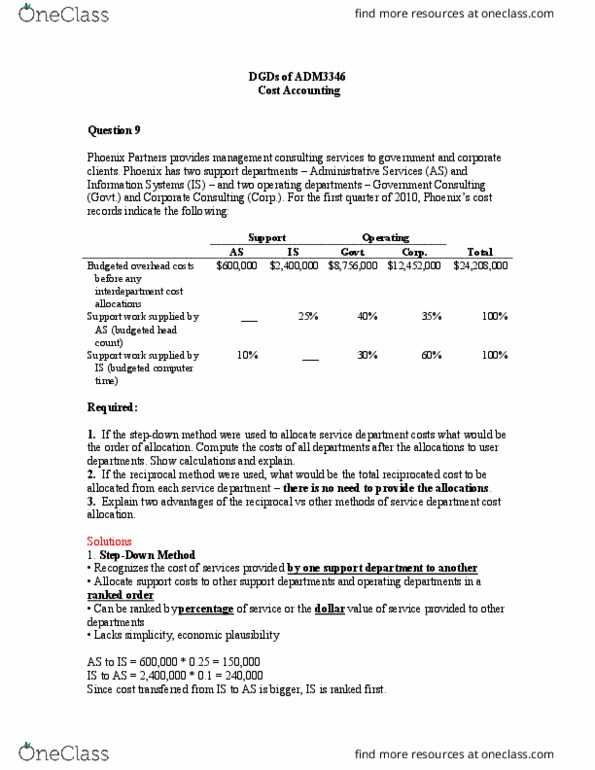

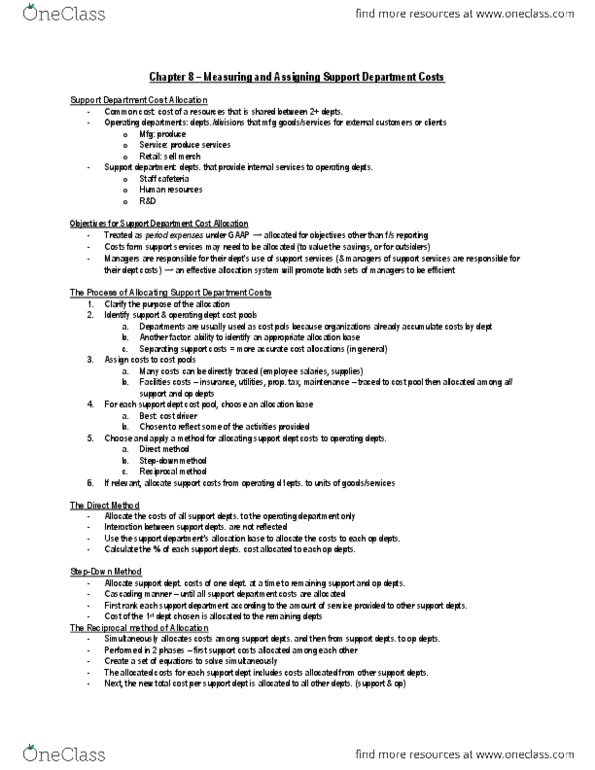

Lo1 define support departments, and explain why their costs are allocated to other departments. Lo2 explain the process that is used to allocate support department costs. Lo3 explain how the direct method is used to allocate support costs to operating departments; calculate cost allocations using the direct method. Lo4 explain how the step-down method is used to allocate support costs to operating departments; calculate cost allocations using the step-down method. Lo5 explain how the reciprocal method is used to allocate support costs to operating departments; calculate cost allocations using the reciprocal method. Lo6 explain the difference between single-and dual-rate allocations. Identify how support cost allocations and information quality impact management decision-making. These learning questions (lo1 through lo7) are cross-referenced in the textbook to individual exercises and problems. All of the methods allocate support department costs to operating. All of the methods rely on allocation bases to assign costs of support departments to operating departments.