Business - Marketing ACC120 Chapter Notes - Chapter 5: Interest Expense, Profit Margin, Income Statement

6 Apr 2014

School

Department

Professor

Document Summary

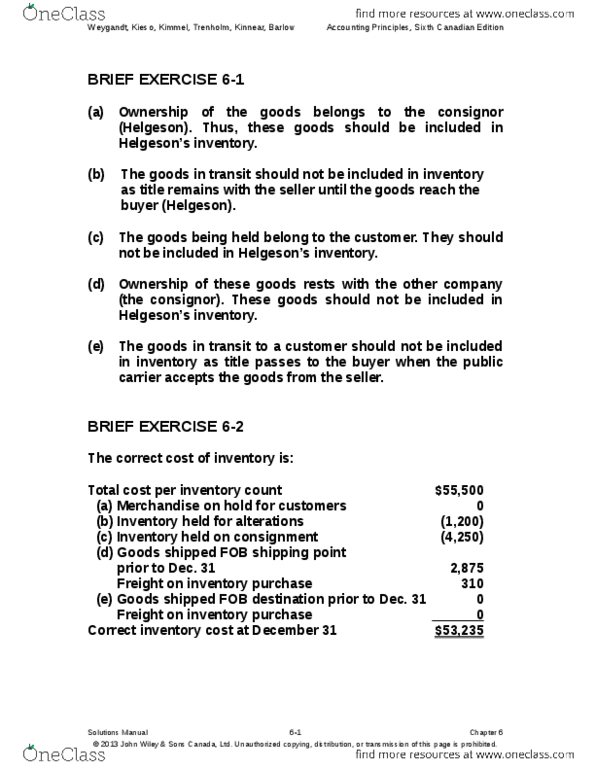

11 accounts payable (,000 ,000) 11,000. Cost of goods available for sale (d) Cost of goods available for sale (above) Note: freight-out is not included; it is an operating expense. 22 (fob destination point means the seller pays the freight, therefore no entry required here. ) 31 accounts payable (,000 ) 12,600. 2 (fob shipping point means the buyer pays the freight, therefore no entry required here. ) May 4 accounts payable (,000 ,800) 10,200. May 4 cash (,000 ,800) 10,200. Exercise 5-13 (a) dec. 3 accounts receivable 32,000 (b) dec. 3 purchases 32,000. Problem 5-6a (a) aug. 31cost of goods sold 2,440 (b) Net sales (,360 ,700 ,440) ,220. Cost of goods sold (,680 + ,440) ,120. Cost of goods sold (,680 + ,440) Profit $ 75,765 (d) gross profit margin = ,100 ,220 = 16. 5% Profit margin = ,765 ,220 = 11. 1% The gross profit margin has deteriorated significantly from 20% in 2013 to 16. 5% in 2014.