BUS 251 Chapter Notes - Chapter 3: Accounting Information System, Retained Earnings, General Ledger

15 Aug 2016

School

Department

Course

Professor

Document Summary

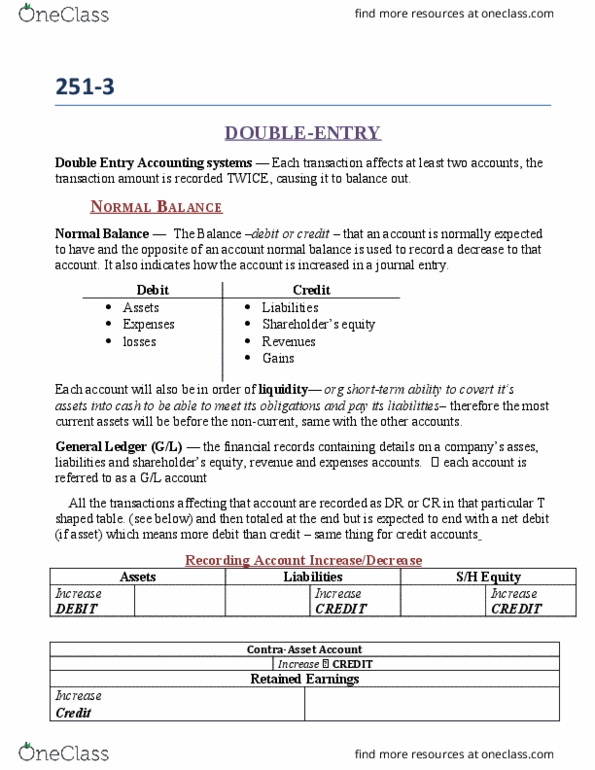

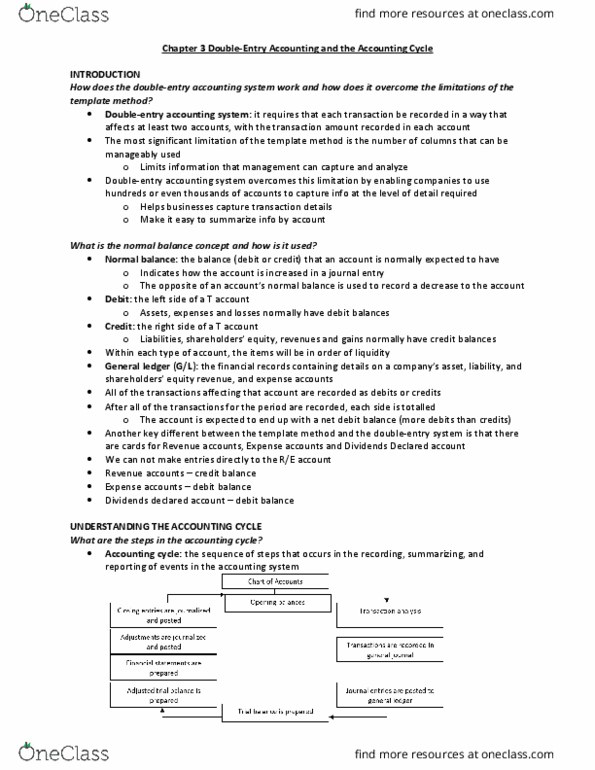

3 double-entry accounting and the accounting cycle. Double-entry accounting system = each transaction must be recorded so that at least 2 accounts affected, w/ transaction amount recorded in each account. Total effects of these entries equal and offsetting. Enables companies to use hundreds/thousands of accounts (columns) to capture info req, while making it easy to summarize info by account. Normal balance concept = accounts on left side of t (asset accounts) normally have debit balance, while accounts on right side (liabilities & shareholders" equity accounts) normally have credit balance. Most current assets/liab come before non-current assets/liab. General ledger = complete record of financial info, contains all accounts. Revenue retained earnings b/c net income and thus r/e. Expenses retained earnings b/c net income and thus r/e. Dividends declared retained earnings b/c are distribution of r/e. Accounting cycle = whole sys by which transactions measured, recorded, summarized & then communicated to users thru financial statements.