BUS 254 Chapter Notes - Chapter 7: Contribution Margin, Total Absorption Costing, Fixed Cost

13 May 2016

School

Department

Course

Professor

3

BUS 254 Full Course Notes

Verified Note

3 documents

Document Summary

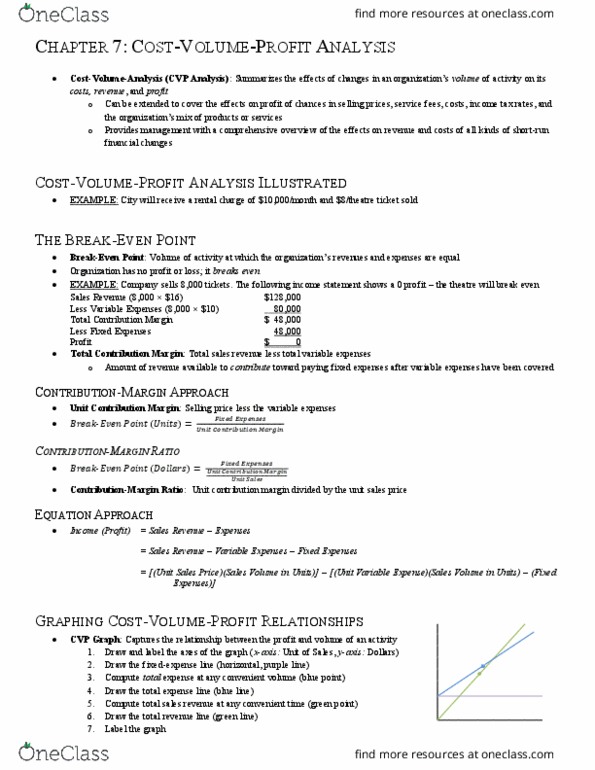

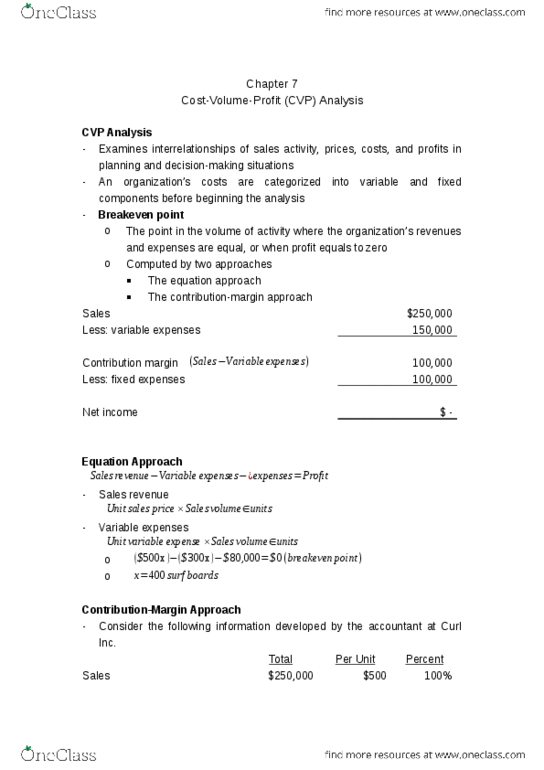

Cost-volume-profit analysis: the technique that summarizes the effects of changes in an organization"s volume of activity on its costs, revenue, and profit. Can also be extended to cover the effects on profit of changes in selling prices, esrvice fees, costs, income tax rates and the organization"s mix of products or services. The effects on revenue and costs by short run financial changes. Not limited to profit: can also be used to asses changes on revenue and costs: cost-volume-profit analysis illustrated (pager 249) Analyzing an organization"s cost behaviour (fixed, variable, mixed) is a necessary first step in any cvp analysis: the break even point (page 250) Break even point: the volume of activity at which the organization"s revenues and expenses are equal. Total contribution margin: total sales revenue total variable expenses. This is the amount of revenue that is available to contribute toward paying fixed expenses after all variable expenses have been covered.