BUS 329 Chapter Notes - Chapter 5: Car Dealership, Capital Cost, British Rail Class 53

14 Oct 2016

School

Department

Course

Professor

Document Summary

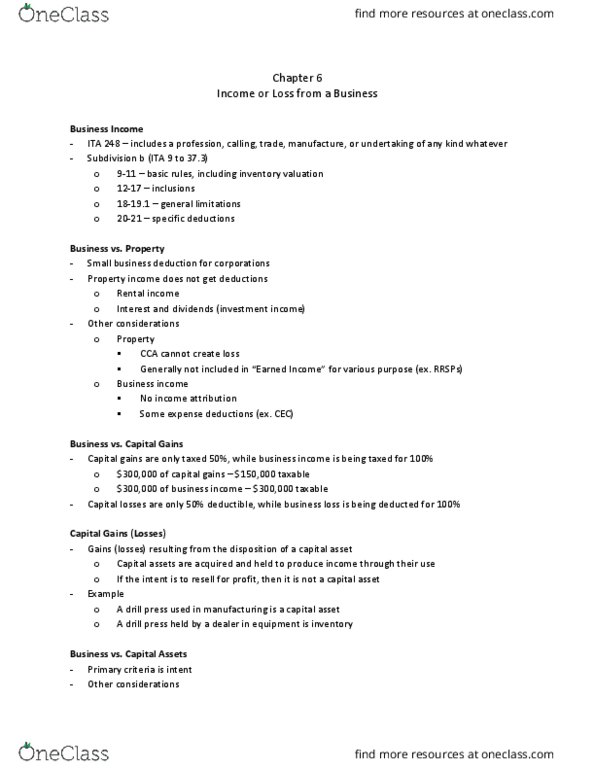

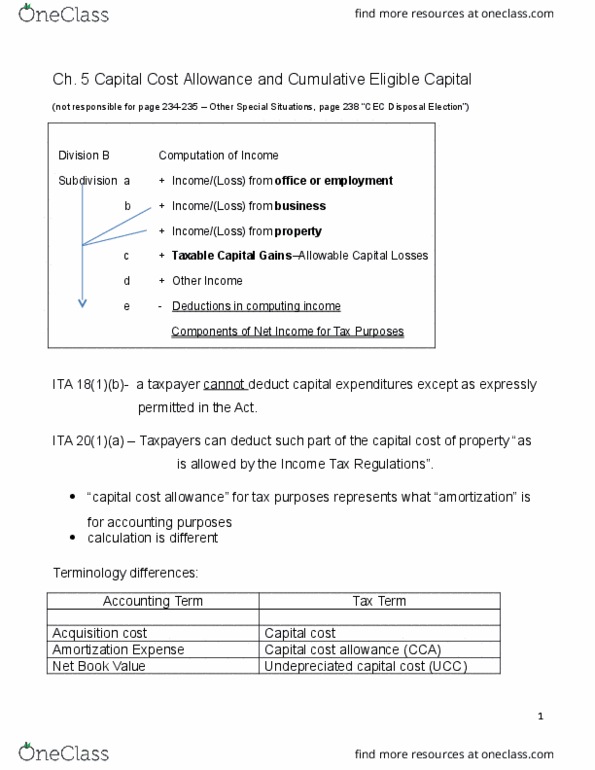

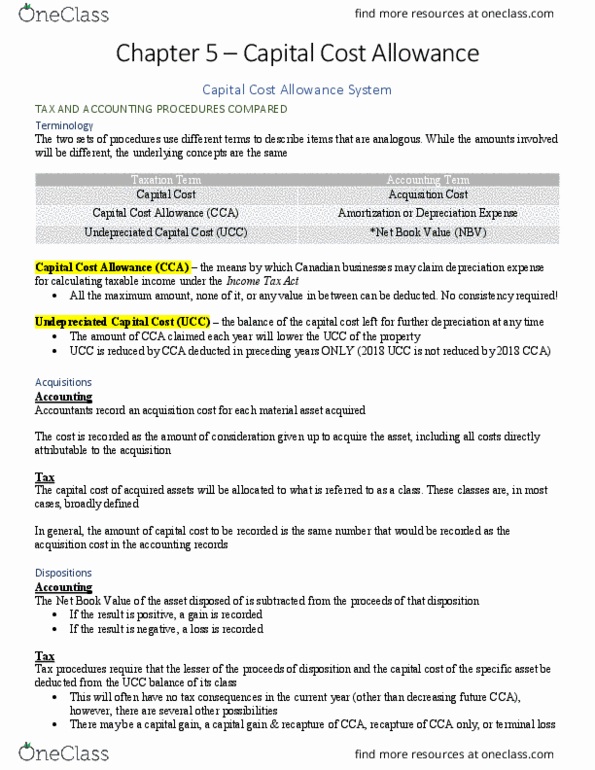

Ita 18(1)(b) prohibits deduction of capital costs. Cca and amortization cca helps to do the deductions. Undepreciated capital cost (ucc) and net book value (nbv) Individual assets in accounting and aggregated classes for tax. Variety of methods straight line method, declining balance, etc. Subtract lesser of capital cost or proceeds of disposition (pod) from class. Recapture, terminal loss, capital gain, or no tax effect. Usual accounting additions (installation and taxes, etc. ) Usually it is for a business, which they rarely choose to include. Transfer between related parties at a price lower than fmv. At the second taxation year after year of acquisition, you have to start calculating cca. Public companies first year amortization is taken. 10% if 90% or more for manufacturing and processing (m&p) 6% if 90% or more for non-residential (commercial buildings) Miscellaneous tangible including communications equipment (ex. non-smart telephones) Passenger vehicles with cost of ,000 or less. Vehicles that are given to sales, executives, and employees, etc.