BUS 426 Chapter Notes - Chapter 7: Audit Evidence, Audit Risk, Internal Control

19 Sep 2012

School

Department

Course

Professor

Document Summary

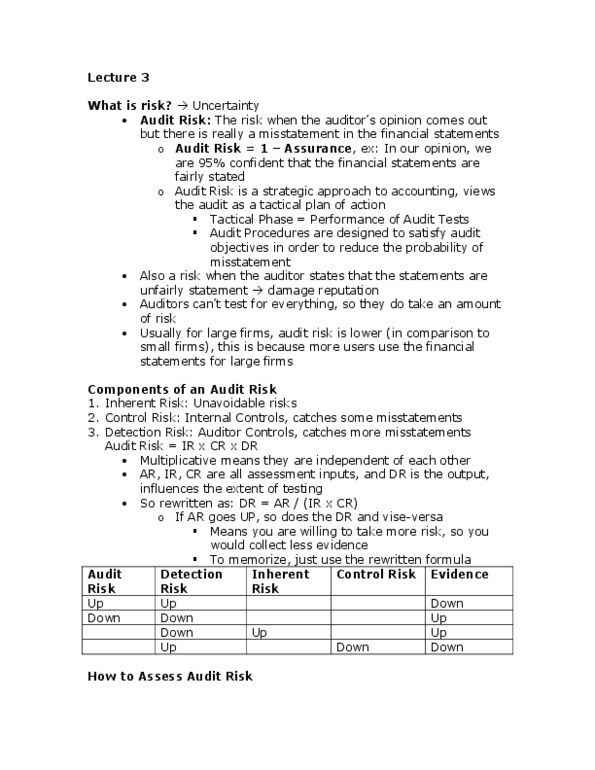

Risk means the acceptance by auditors that there is some level of uncertainty in performing the audit function. Audit risk model: a formal model reflecting the relationships among audit risk (ar), inherent risk (ir), control risk (cr) and planned detection (pd) Ar = ir x cr x pdr. Mainly used to decide how much evidence to accumulate in each cycle. Cr: if pdr = 2%, then auditor needs to provide 98% assurance. Auditor plans 2 percent risk of not detecting errors and so seeks 98 percent assurance from substantive tests . See page 210 for relationship of these risks. The likelihood is that if the client goes bankrupt after the audit, they may sue the auditors. Factors that affect business risks: the degree to which external users rely on the statements. Larger the client size, more widely used the statements.