ADMN 3221H Chapter Notes - Chapter 3: Capital Account, Accounts Receivable, Income Statement

4 Oct 2017

School

Department

Course

Professor

Document Summary

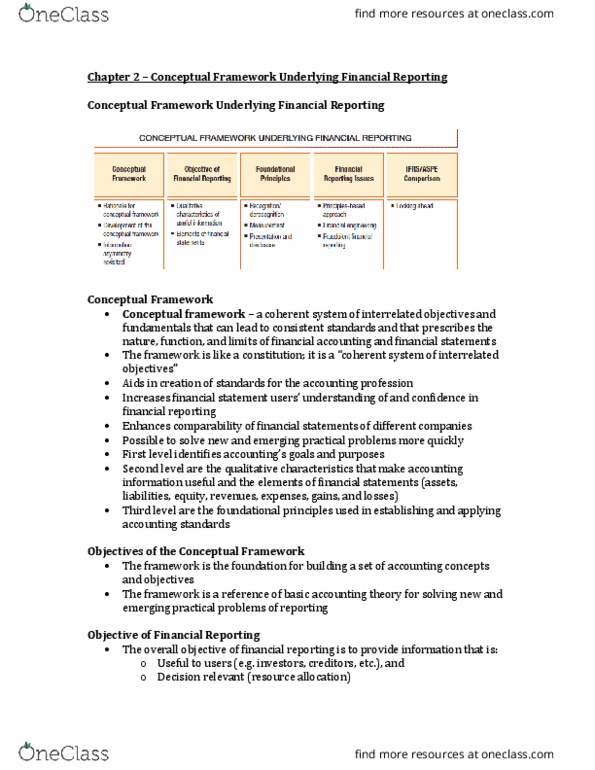

Chapter 3 the accounting information system and measurement issues. Accounting information system the system for collecting and processing transaction data to make financial information available to interested parties. The accounting equation: assets = liabilities + shareholders" equity, shareholders" equity = common shares + retained earnings dividends + Revenues expenses: assets = liabilities + common shares + retained earnings dividends + Company paid ,000 for one-year insurance when coverage begins october 1 and debited prepaid insurance for ,000: unearned revenues revenue received in cash and recorded as liabilities, ex. Company received (cid:884),(cid:882)(cid:882)(cid:882) for four months" advertising services that begins oct. 1. ,000 was credited to unearned revenue before being earned. The closing process account called income summary: revenues and expenses are matched in the income summary account, this is then transferred to equity account (retained earnings, etc. ) In a perpetual inventory system, purchases and sales are recorded directly in the inventory account as they occur: no adjusting entries are needed.