ADMN 4303H Chapter Notes - Chapter 8: Cash Flow Statement, Amortization Schedule, Cash Flow

30 Mar 2020

School

Department

Course

Professor

Document Summary

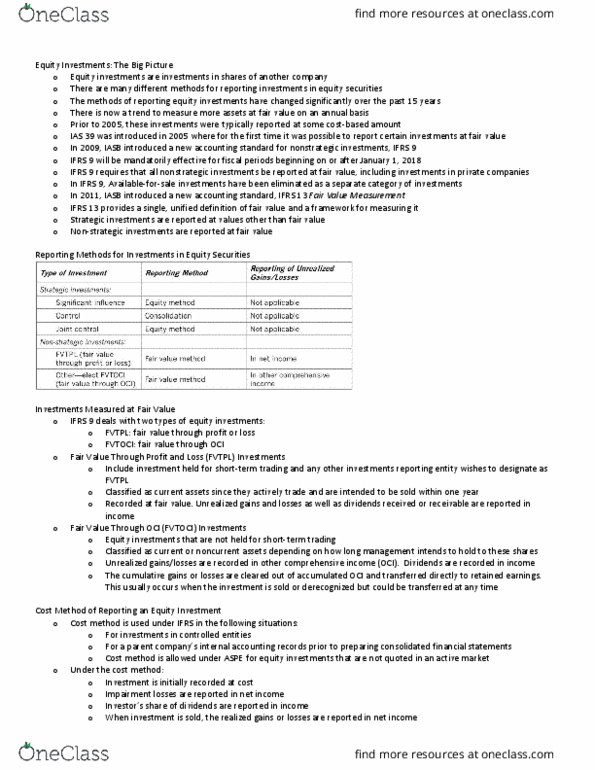

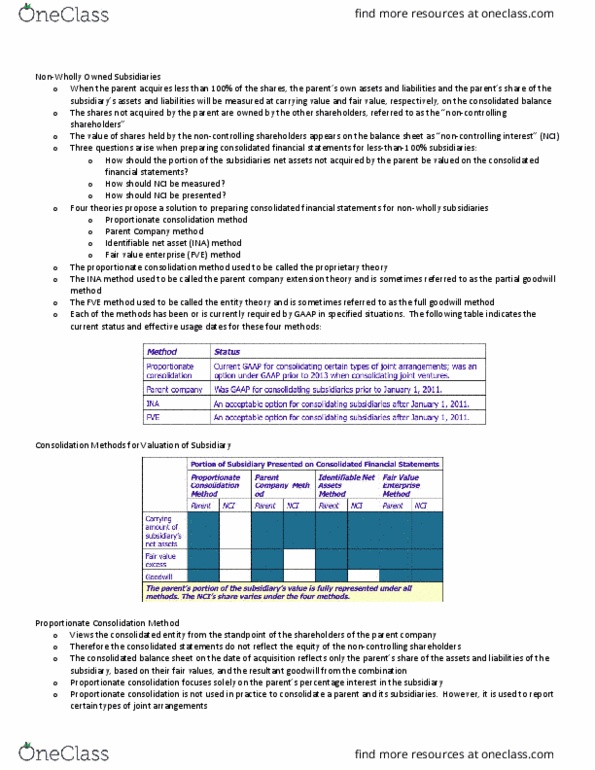

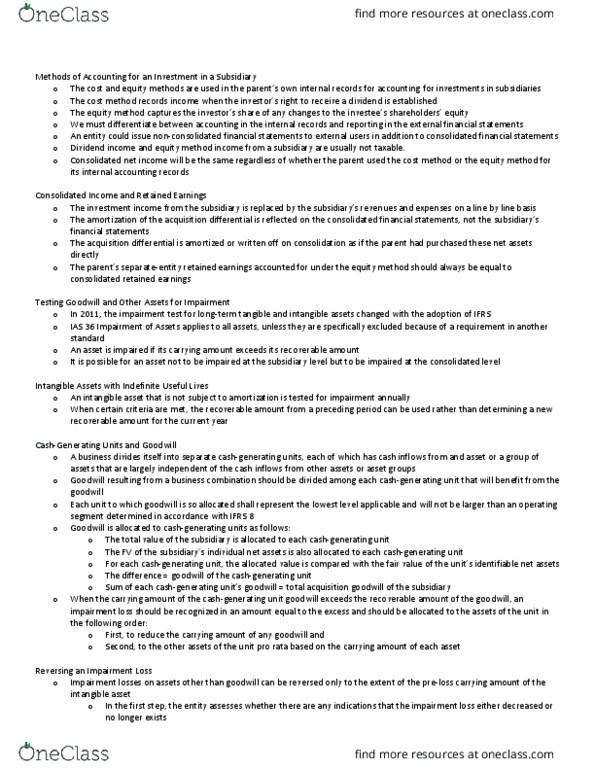

Dividends paid by subsidiaries to non-controlling shareholders are disclosed separately from dividends paid by the parent to its shareholders. In the period that a subsidiary is acquired: cash paid to acquire the subsidiary, less cash held by the subsidiary, is netted and disclosed on one line under. Investing activities on the cash flow statement as: For this calculation, the amount paid equals the carrying value of previous purchases + cost of the current purchase. For additional acquisitions that occur after control has been obtained: do not calculate a separate ad. Instead, treat the acquisition as a transfer of equity from non-controlling interest to the parent with the following calculation: balance sheet non-controlling interest amount prior to the acquisition x portion sold to the parent = If the cost of the step acquisition is greater than amount of the transfer from nci, the difference is debited to consolidated retained earnings. Indirect shareholdings: the following diagrams illustrate both direct and indirect holdings.