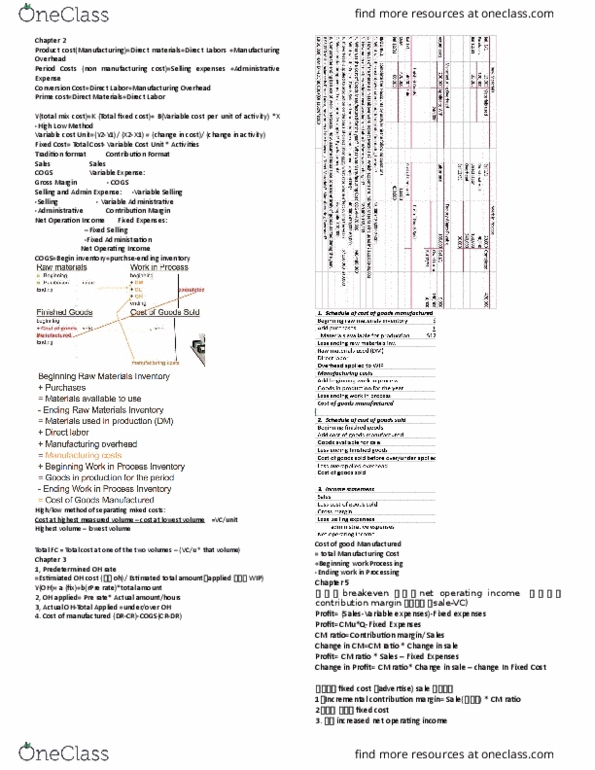

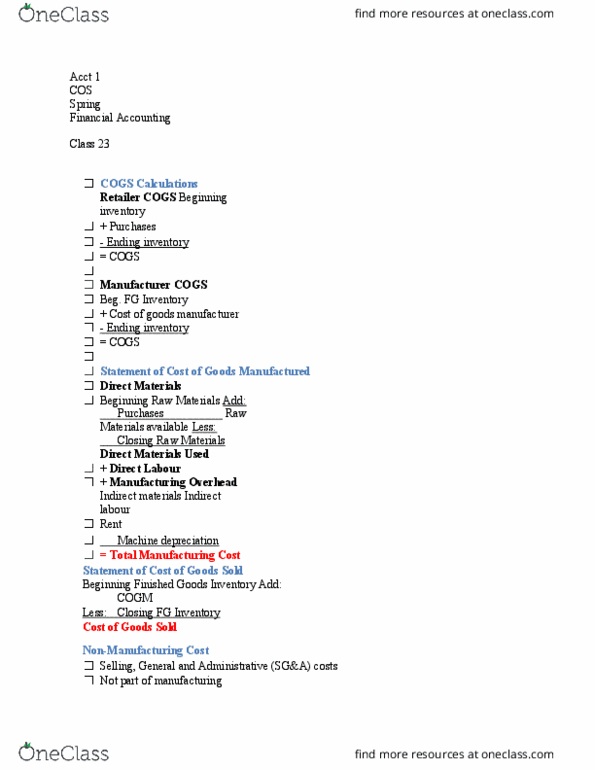

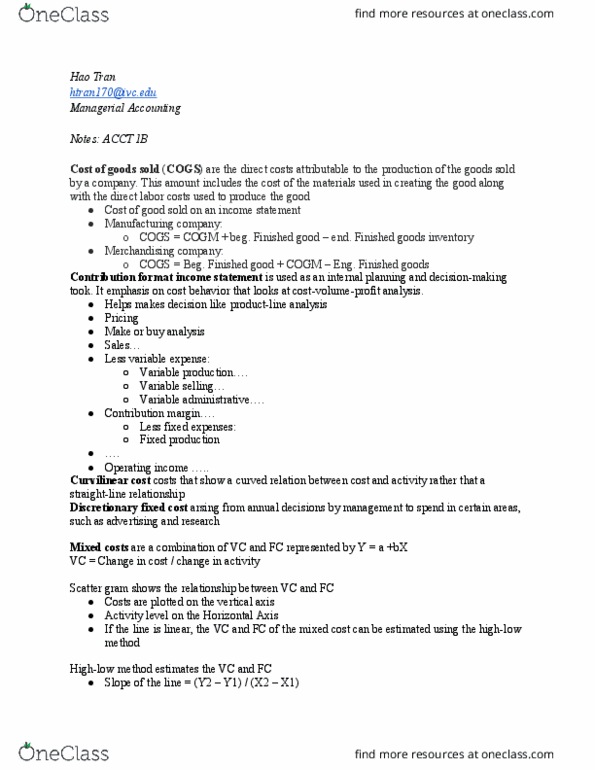

MGT 3100 Chapter Notes - Chapter 6: Contribution Margin, Variable Cost

Chapter 6-Cost Behaviour Part 2

TRADITIONAL INCOME STATEMENT

• Traditional income statements are organized by function not by cost behaviour.

• Costs relating to production or purchases are recorded to COGS above the gross profit

line when they are sold.

• All other costs appear as operating expenses below the gross profit line.

• COGS is a variable cost for a retailer, but is a mixed cost for manufactures.

Generally VC since a change in units results in a

change in # of workers

Includes VC like indirect materials and indirect

labour and FC like property taxes and insurance.

CONTRIBUTION MARGIN INCOME STATEMENTS

• Contribution margin statements enable managers to quickly determine how costs will

change with volume and which will remain fixed.

• Arrange cost by behaviour rather than function

• Changes in volume will affect total sales revenue and total variable costs and,

changing the contribution margin

• Changes in volume will not affect fixed costs within the same relevant range

• Distinguishes the figures that will change from those that will not change with changes

in volume

• Can only be used internally since they are not acceptable for external reporting under

IFRS and ASPE

• Present all variable costs above the contribution margin line. Including:

• Any variable costs in merchandise sold or selling and admin

• Present all fixed costs below the contribution margin line.

• Any fixed costs relating to merchandise sold or selling and admin

• Contribution margin is equal to:

Sales Revenue-Variable Cost

• The challenge for creating a contribution margin statement is dealing with mixed costs.

• Mixed costs need to be separated into their fixed and variable portions.

Direct Materials

Direct Labour

Manufacturing

overhead

Inventoriable

product costs

+

+

=

A variable cost

Generally treated as a

variable cost

A mixture of fixed

and variable costs

A mixture of fixed

and variable costs

find more resources at oneclass.com

find more resources at oneclass.com