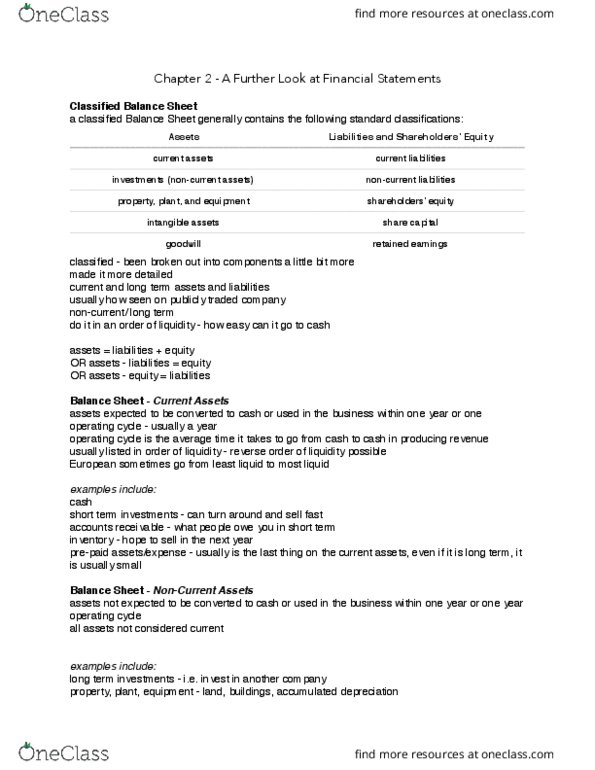

ACCTG300 Chapter Notes - Chapter 2: Accounts Payable, Promissory Note, Current Liability

Document Summary

Get access

Related Documents

Related Questions

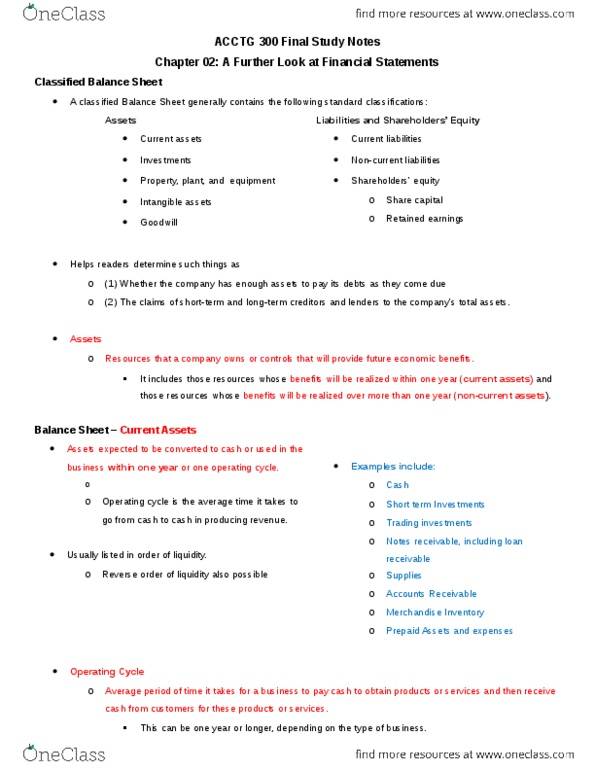

The comparative statements of financial position of Mikos Inc. as at December 31, 2017 and 2018, and its statement of earnings for the year ended December 31, 2018, are presented below:

| MIKOS INC. | ||||||

| Comparative Statements of Financial Position | ||||||

| December 31 | ||||||

| 2018 | 2017 | |||||

| Assets | ||||||

| Cash | $ | 10,600 | $ | 18,600 | ||

| Short-term investments | 72,200 | 40,800 | ||||

| Accounts receivable | 76,000 | 32,400 | ||||

| Inventories, at cost | 57,200 | 41,600 | ||||

| Prepaid expenses | 5,600 | 9,200 | ||||

| Land | 51,400 | 78,000 | ||||

| Property, plant, and equipment, net | 286,400 | 187,000 | ||||

| Intangible assets | 25,600 | 31,200 | ||||

| $ | 585,000 | $ | 438,800 | |||

| Liabilities and Shareholdersâ Equity | ||||||

| Accounts payable | $ | 18,600 | $ | 43,200 | ||

| Income tax payable | 9,200 | 2,600 | ||||

| Accrued liabilities | 11,600 | -0- | ||||

| Long-term notes payable | 126,000 | 182,000 | ||||

| Contributed capital | 232,000 | 68,000 | ||||

| Retained earnings | 187,600 | 143,000 | ||||

| $ | 585,000 | $ | 438,800 | |||

| MIKOS INC. | |||||

| Statement of Earnings | |||||

| For the Year Ended December 31, 2018 | |||||

| Sales | $ | 898,000 | |||

| Cost of sales | $ | 446,000 | |||

| Amortization expenseâintangible assets | 5,600 | ||||

| Depreciation expenseâproperty, plant, and equipment | 34,600 | ||||

| Operating expenses | 237,000 | ||||

| Interest expense | 13,600 | 736,800 | |||

| Earnings before income taxes | 161,200 | ||||

| Income tax expense | 48,360 | ||||

| Net earnings | $ | 112,840 | |||

| Additional information is as follows: | |

| a. | Land was sold for cash at its carrying amount. |

| b. | The short-term investments will mature in February 2019. |

| c. | Cash dividends were declared and paid in 2018. |

| d. | New equipment with a cost of $167,600 was purchased for cash, and old equipment was sold at its carrying amount. |

| e. | Long-term notes of $18,000 were paid in cash, and notes of $38,000 were converted to shares. |

| 1. | Prepare a statement of cash flows for Mikos Inc. for the year ended December 31, 2018 by using the indirect method. (Negative answers should be indicated by a minus sign.) |

Basic Financial Ratios

The accounting staff of CCB Enterprises has completed the financial statements for the 2016 calendar year. The statement of income for the current year and the comparative statements of financial position for 2016 and 2015 follow.

| CCB Enterprises | |

| Statement of Income | |

| For the Year Ended December 31, 2016 | |

| (thousands omitted) | |

| Revenue: | |

| Net sales | $794,620 |

| Other | 58,420 |

| Total revenue | $853,040 |

| Expenses: | |

| Cost of goods sold | $530,320 |

| Research and development | 24,480 |

| Selling and administrative | 155,320 |

| Interest | 19,600 |

| Total expenses | $729,720 |

| Income before income taxes | $123,320 |

| Income taxes | 49,328 |

| Net income | $73,992 |

| CCB Enterprises | ||

| Comparative Statements of Financial Position | ||

| December 31, 2016 and 2015 | ||

| (thousands omitted) | ||

| 2016 | 2015 | |

| Assets | ||

| Current assets: | ||

| Cash and short-term investments | $25,910 | $20,860 |

| Receivables, less allowance for doubtful accounts | ||

| ($1,130 in 2016 and $1,410 in 2015) | 48,190 | 50,300 |

| Inventories, at lower of FIFO cost or market | 64,860 | 62,100 |

| Prepaid items and other current assets | 5,220 | 3,280 |

| Total current assets | $144,180 | $136,540 |

| Other assets: | ||

| Investments, at cost | $105,880 | $105,880 |

| Deposits | 10,160 | 7,980 |

| Total other assets | $116,040 | $113,860 |

| Property, plant, and equipment: | ||

| Land | $12,100 | $12,100 |

| Buildings and equipment, less accumulated depreciation | ||

| ($126,330 in 2016 and $122,240 in 2015) | 268,840 | 247,870 |

| Total property, plant, and equipment | $280,940 | $259,970 |

| Total assets | $541,160 | $510,370 |

| Liabilities and Ownersâ Equity | ||

| Current liabilities: | ||

| Short-term loans | $22,180 | $23,900 |

| Accounts payable | 72,240 | 71,070 |

| Salaries, wages, and other | 26,300 | 26,780 |

| Total current liabilities | $120,720 | $121,750 |

| Long-term debt | $160,620 | $171,030 |

| Total liabilities | $281,340 | $292,780 |

| Ownersâ equity: | ||

| Common stock, at par | $43,840 | $42,010 |

| Paid-in capital in excess of par | 64,020 | 61,260 |

| Total paid-in capital | $107,860 | $103,270 |

| Retained earnings | 151,960 | 114,320 |

| Total ownersâ equity | $259,820 | $217,590 |

| Total liabilities and ownersâ equity | $541,160 | $510,370 |

Required:

1. Calculate the following financial ratios for 2016 for CCB Enterprises:

Round items h, j, and k to the nearest whole number. Round all other answers to two decimal places. Assume a 360-day year.

| a. Times interest earned | to 1 |

| b. Return on total assets | % |

| c. Return on common stockholders' equity | % |

| d. Debt-to-equity ratio (at December 31, 2016) | to 1 |

| e. Current ratio (at December 31, 2016) | to 1 |

| f. Quick (acid-test) ratio (at December 31, 2016) | to 1 |

| g. Accounts receivable turnover ratio (Assume that all sales are on credit.) | times |

| h. Number of days' sales in receivables | days |

| i. Inventory turnover ratio (Assume that all purchases are on credit.) | times |

| j. Number of days' sales in inventory | days |

| k. Number of days in cash operating cycle | days |

2. Which of the following statements pertaining to ratio analysis of CCB Enterprises is true?

All of these are true.

I need these ratios:

Return on Assets

|