MGST 217 Chapter Notes - Chapter 16: Retained Earnings, Income Statement, Accounts Payable

19 Oct 2016

School

Department

Course

Professor

2

MGST 217 Full Course Notes

Verified Note

2 documents

Document Summary

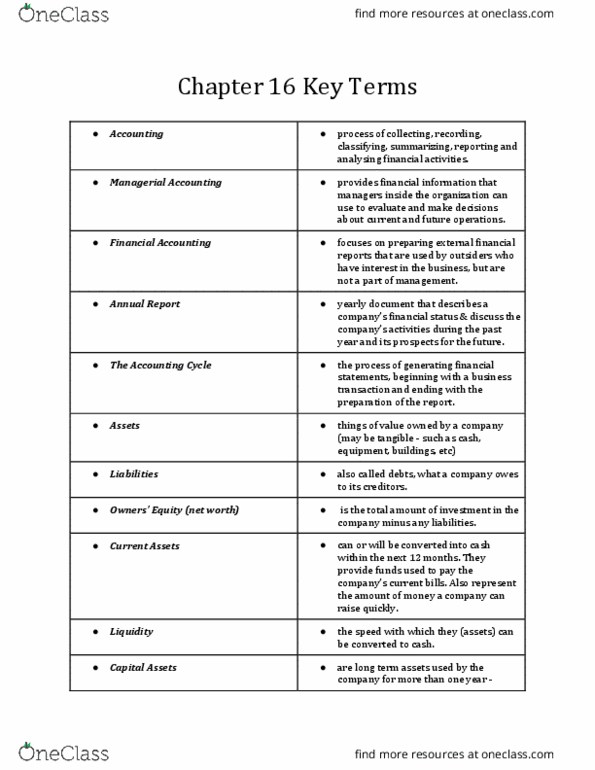

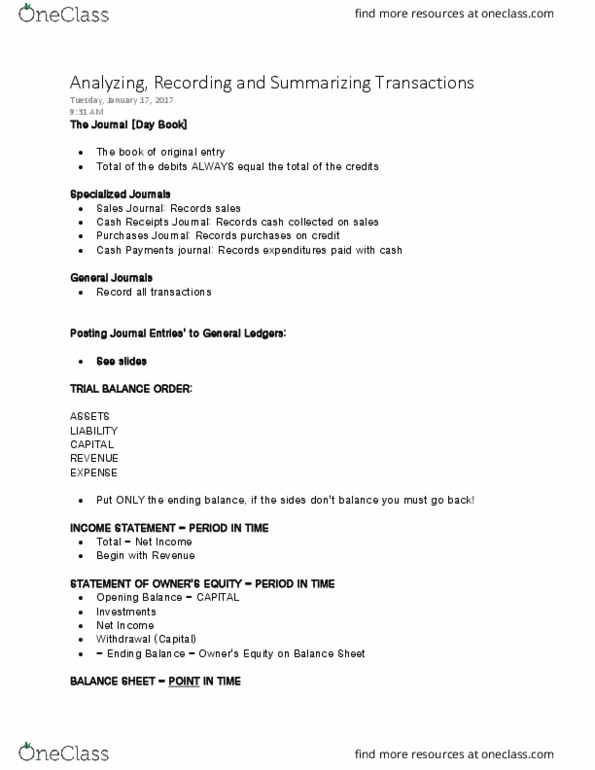

Analyze data collected from many different sources. Accounts for any transaction that has a financial impact in the company. Transactions are recorded in journals which are in turn kept in ledgers, the summary of the ledgers is represented in a trial balance: the accounting equation. Liabilities is what you owe, also known as debts. Owner"s equity is the total amount of investments in the company. To balance the equation each entry is recorded in two parts, an equal and opposite transaction, this method is known as double entry bookkeeping: the t-account. Used to analyze financial transactions, named by its shape resembling a t. Left side of the t is the debit record. Right side of the t is the credit record. The rule is that a rise on one side of the t corresponds to an equal decrease in the other side of the t: the trial balance. A list of each account and its net balance.