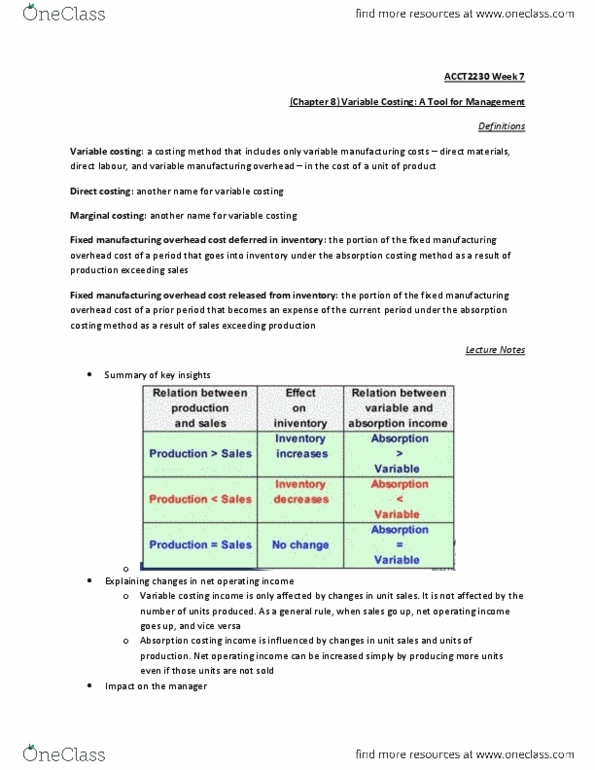

ACCT 2230 Chapter Notes - Chapter 8: Activity-Based Costing, Earnings Before Interest And Taxes, Fixed Cost

Document Summary

Get access

Related Documents

Related Questions

***The last person who answered, did not answer the questions in format. Please provide the answers for the required fields on the chart. Label the answers please or list them in a chart like the ones provided in the question.***

*CHECK NUMBERS; PLEASE PROVIDE AN EXPLAINATION FOR EACH AND ANSWER EACH PART FOR QUESTIONS #1-#3 WITH FORMULAS*

Tami Tyler opened Tamiâs Creations, Inc., a small manufacturing company, at the beginning of the year. Getting the company through its first quarter of operations placed a considerable strain on Ms. Tylerâs personal finances. The following income statement for the first quarter was prepared by a friend who has just completed a course in managerial accounting at State University.

| Tamiâs Creations, Inc. Income Statement For the Quarter Ended March 31 | |||||||

| Sales (22,000 units) | $ | 798,600 | |||||

| Variable expenses: | |||||||

| Variable cost of goods sold | $ | 257,400 | |||||

| Variable selling and administrative expenses | 176,000 | 433,400 | |||||

| Contribution margin | 365,200 | ||||||

| Fixed expenses: | |||||||

| Fixed manufacturing overhead | 202,500 | ||||||

| Fixed selling and administrative expenses | 218,000 | 420,500 | |||||

| Net operating loss | $ | ( 55,300 | ) | ||||

Ms. Tyler is discouraged over the loss shown for the quarter, particularly because she had planned to use the statement as support for a bank loan. Another friend, a CPA, insists that the company should be using absorption costing rather than variable costing and argues that if absorption costing had been used the company probably would have reported at least some profit for the quarter.

At this point, Ms. Tyler is manufacturing only one product, a swimsuit. Production and cost data relating to the swimsuit for the first quarter follow:

| Units produced | 25,000 | ||

| Units sold | 22,000 | ||

| Variable costs per unit: | |||

| Direct materials | $ | 7.20 | |

| Direct labor | $ | 2.70 | |

| Variable manufacturing overhead | $ | 1.80 | |

| Variable selling and administrative | $ | 8.00 | |

Required:

1. Complete the following:

a. Compute the unit product cost under absorption costing. (Round your intermediate and final answers to 2 decimal places.)

Unit Product Cost:_______________

b. Redo the companyâs income statement for the quarter using absorption costing. (Round your intermediate calculations to 2 decimal places.)

| |||||||||||||||||||

+

c. Reconcile the variable and absorption costing net operating income (loss) figures. (Round your intermediate calculations to 2 decimal places.)

| ||||||||||

+

3. During the second quarter of operations, the company again produced 25,000 units but sold 28,000 units. (Assume no change in total fixed costs.)

a. Prepare a contribution format income statement for the quarter using variable costing. (Round your intermediate calculations to 2 decimal places.)

| ||||||||||||||||||||||||||||||||||||||||||||||||||

+

b. Prepare an income statement for the quarter using absorption costing. (Round your intermediate calculations to 2 decimal places.)

| |||||||||||||||||||

+

c. Reconcile the variable costing and absorption costing net operating incomes. (Round your intermediate calculations to 2 decimal places.)

| Reconciliation of Variable Costing and Absorption Costing Net Operating Incomes (Losses) | ||

| Variable costing net operating income (loss) | ||

| Absorption costing net operating income (loss) | ||

Tami Tyler opened Tamiâs Creations, Inc., a small manufacturing company, at the beginning of the year. Getting the company through its first quarter of operations placed a considerable strain on Ms. Tylerâs personal finances. The following income statement for the first quarter was prepared by a friend who has just completed a course in managerial accounting at State University.

| Tamiâs Creations, Inc. Income Statement For the Quarter Ended March 31 | ||||||

| Sales (23,000 units) | $ | 834,900 | ||||

| Variable expenses: | ||||||

| Variable cost of goods sold | $ | 271,400 | ||||

| Variable selling and administrative | 177,100 | 448,500 | ||||

| Contribution margin | 386,400 | |||||

| Fixed expenses: | ||||||

| Fixed manufacturing overhead | 213,200 | |||||

| Fixed selling and administrative | 220,000 | 433,200 | ||||

| Net operating loss | $ | ( 46,800) | ||||

Ms. Tyler is discouraged over the loss shown for the quarter, particularly because she had planned to use the statement as support for a bank loan. Another friend, a CPA, insists that the company should be using absorption costing rather than variable costing and argues that if absorption costing had been used the company probably would have reported at least some profit for the quarter.

At this point, Ms. Tyler is manufacturing only one productâa swimsuit. Production and cost data relating to the swimsuit for the first quarter follow:

| Units produced | 26,000 | |||

| Units sold | 23,000 | |||

| Variable costs per unit: | ||||

| Direct materials | $ | 7.20 | ||

| Direct labor | $ | 3.00 | ||

| Variable manufacturing overhead | $ | 1.60 | ||

| Variable selling and administrative | $ | 7.70 | ||

Required:

1. Complete the following:

a. Compute the unit product cost under absorption costing.

b. What is the companyâs absorption costing net operating income (loss) for the quarter?

c. Reconcile the variable and absorption costing net operating income (loss) figures.

3. During the second quarter of operations, the company again produced 26,000 units but sold 29,000 units. (Assume no change in total fixed costs.)

a. What is the companyâs variable costing net operating income (loss) for the second quarter?

b. What is the companyâs absorption costing net operating income (loss) for the second quarter?

c. Reconcile the variable costing and absorption costing net operating incomes for the second quarter.