ACCT 2230 Chapter : Managerial Accounting Chapter Three Notes

14 Jan 2012

School

Department

Course

Professor

Document Summary

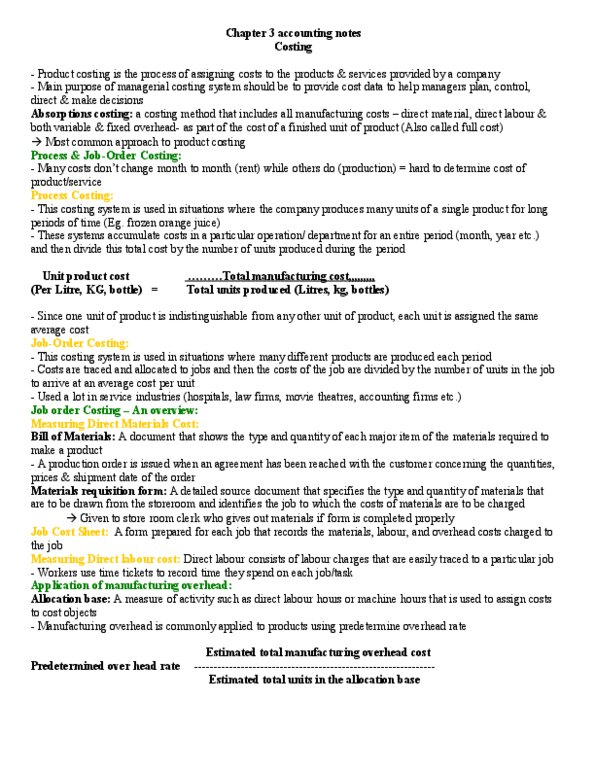

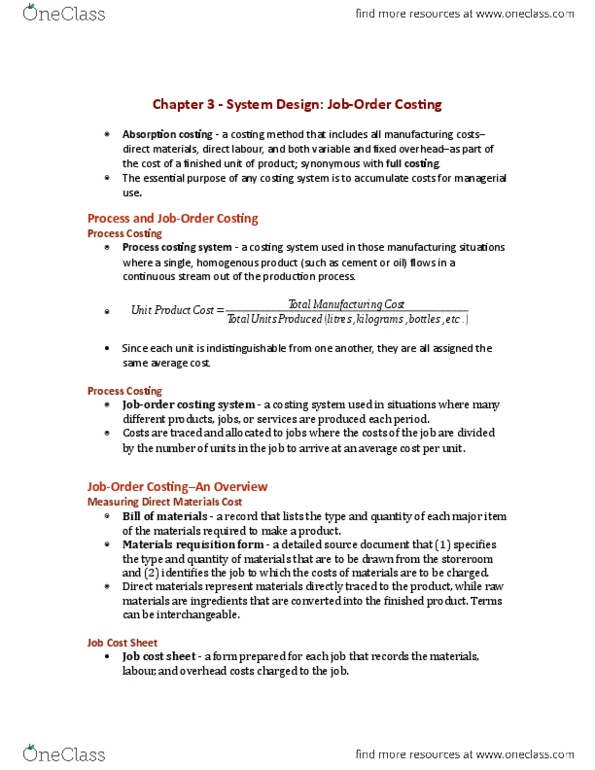

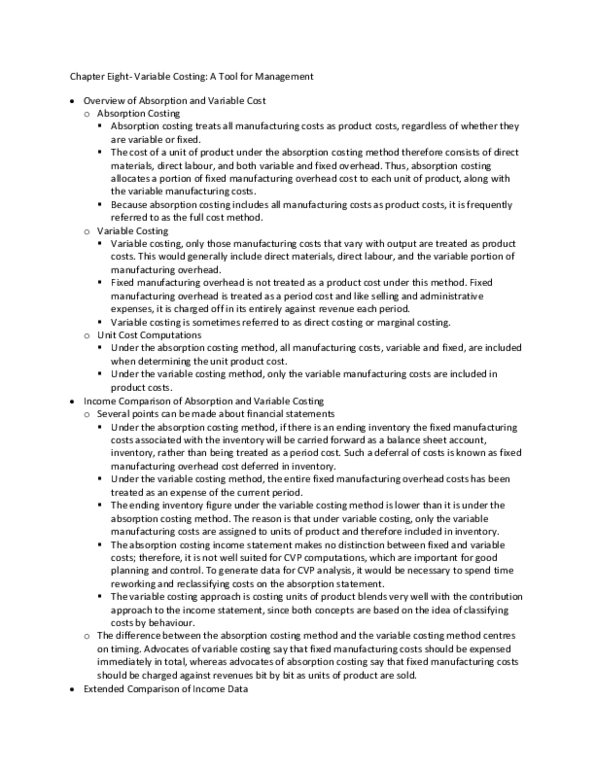

Absorption costing is all manufacturing costs, fixed and variable, are signed to units of product unit are said to fully absorb manufacturing costs. The absorption costing approach is also known as the full cost approach. y we must keep in mind that the essential purpose of any costing system is to accumulate costs for managerial use. More sophistication yields more benefit by providing more relevant information. a process costing system is a costing system used in those manufacturing situations where a single, homogeneous product (such as cement or flour) is produced for long periods of time. process costing systems accumulate costs in a particular operating or department for an entire period (month, quarter, year) and the divide this total cost by the number of units produced during the period. The basic formula for the process costing is: unit product cost (per litre, kilogram, bottle) = total manufacturing cost / total units produced (litres, kilogram, bottle)