ACCT 2230 Chapter : Managerial Accounting Chapter Eleven Notes

14 Jan 2012

School

Department

Course

Professor

Document Summary

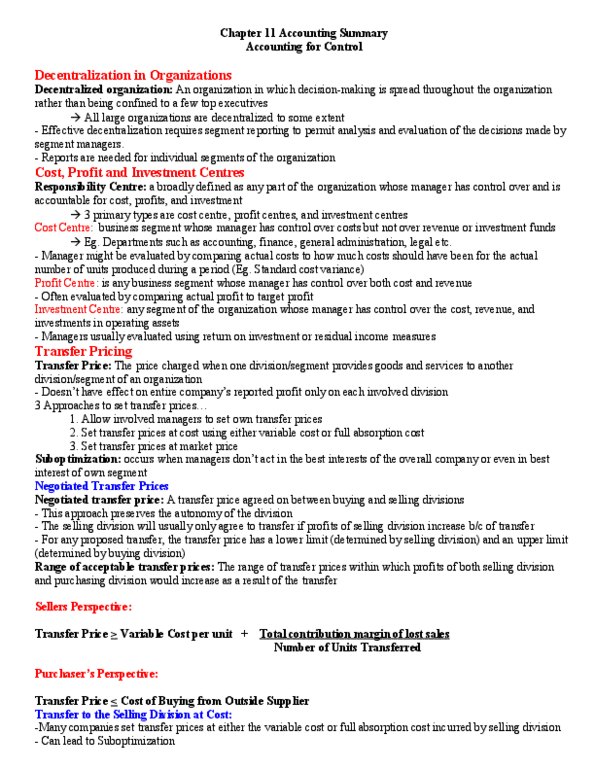

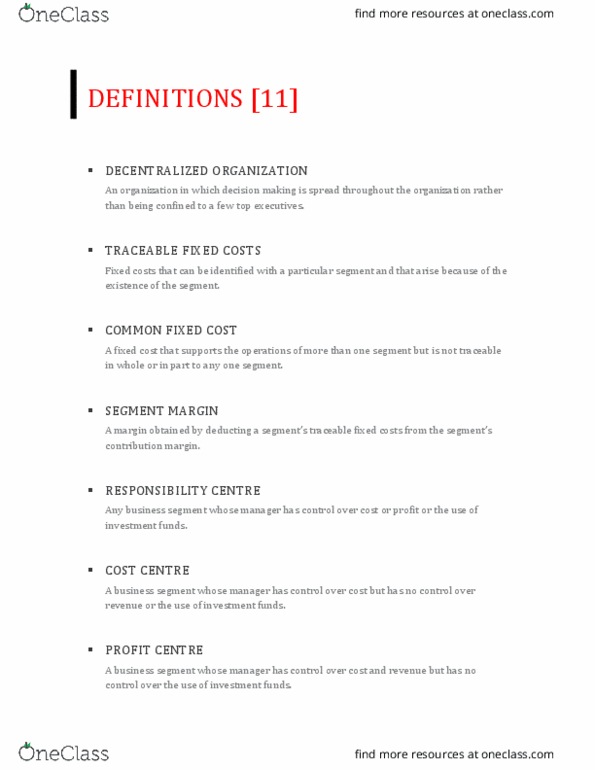

Chapter eleven reporting for control y decentralization in organizations. In a decentralized organization decision making is spread through the organization, rather than being confined to a few top executives: decentralization and segment reporting. a cost centre is a business segment whose manager has control over costs but not over revenue or investment funds. The managers of cost centres are expected to minimized cost while providing the level of services or the amount of products demanded by the other parts of the organization: profit centre. a profit centre is any business segment whose manager has control over both cost and revenue. a profit centre manager generally does not have control over investment funds. profit centre managers are often evaluated by comparing actual profit to targeted or budgeted profit. As a result, managers are intensely interested in how transfer prices are set: three common approaches are used to set transfer prices.